Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

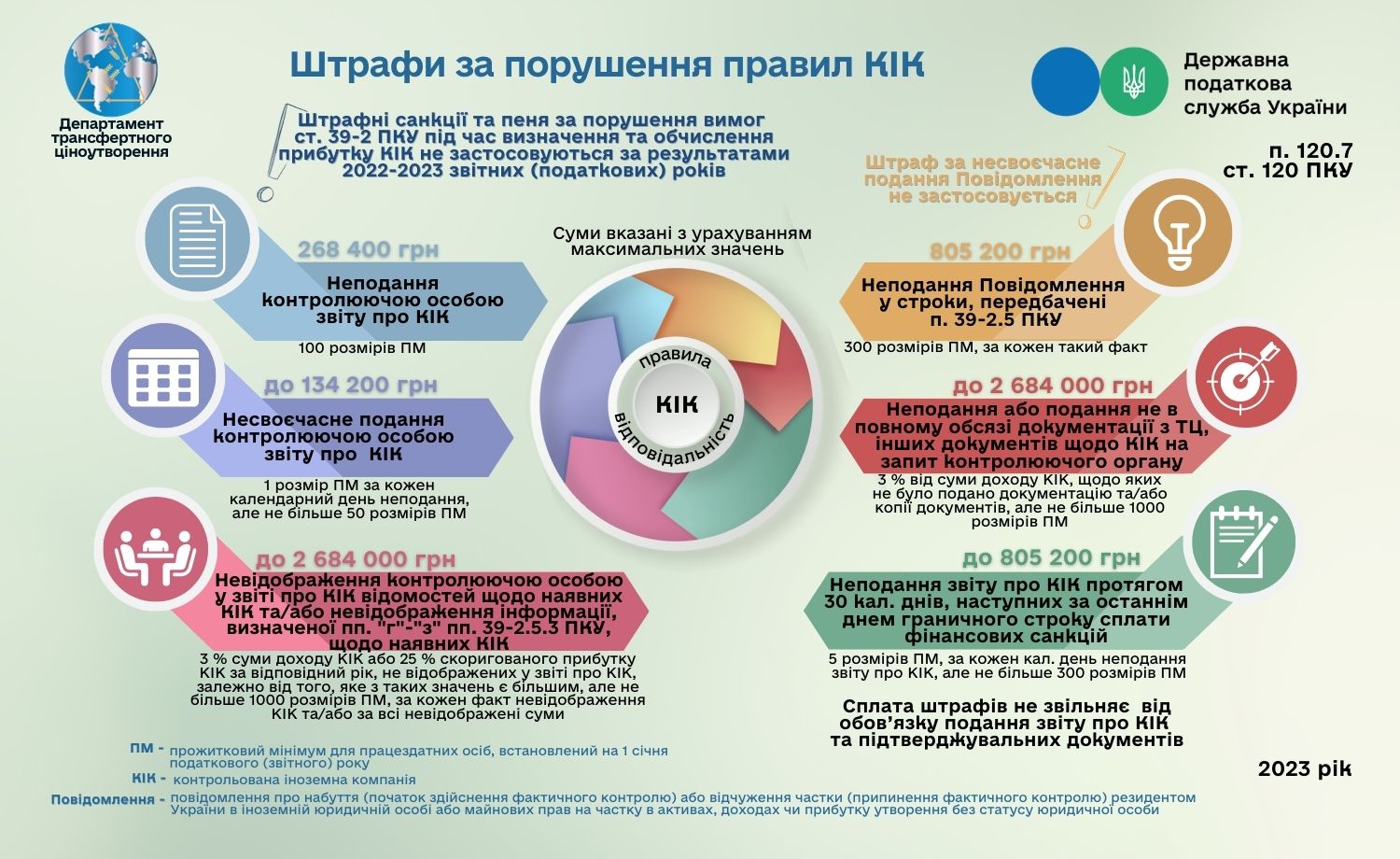

State Tax Service reminds that last year in Ukraine, rules of control over controlled foreign companies were introduced (Laws of Ukraine No. 466-IX as of 16.01.2020 and No. 1117-IX as of 17.12.2020). Starting from January 1, 2022, for opening business abroad, the legal entity or individual resident of Ukraine must prepare and submit:

- information on the acquisition/termination of participation in the controlled foreign companies, in particular, Notification on the acquisition (beginning of actual control) or alienation (termination of actual control) by resident of a share in the foreign legal entity or property rights to a share in assets, income or profit of entity without the legal entity’s status (hereinafter - Notification), form of which was approved by Order of the Ministry of Finance of Ukraine No. 512 as of 22.09.2021;

- annual report on the controlled foreign companies (at the same time as the annual property status and income declaration). Paragraph 54 Sub-section 10 Section XX "Transitional Provisions" of the Tax Code of Ukraine (hereinafter – TCU) establishes application specifics of provisions on the income taxation of controlled foreign companies during the transitional period, in particular, controlling individuals have a right to submit Report for 2022 to the controlling body simultaneously with submission of the annual Declaration for 2023. Herewith, penalties and/or fines are not applied.

Provisions of Article 392 of the TCU stipulate that controlled foreign companies any legal entity registered in a foreign country or territory, which is recognized as being under control of individual or legal entity – resident of Ukraine, according to rules defined by the TCU, is recognized as a controlled foreign company.

Please note that in order to comply with legislative requirements regarding rules of the controlled foreign companies, individuals and legal entities – residents of Ukraine should analyze in detail conditions for owning a share in the foreign company, determine presence or absence of status of the controlling individual of such company and carry out reporting measures provided for in Article 392 of the TCU.

Fulfill your obligations on time so as not to pay significant fines for failure to comply with requirements of Article 392 of the TCU.

Important! Penalties and/or fines are not applied for late submission of the Notification.