Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

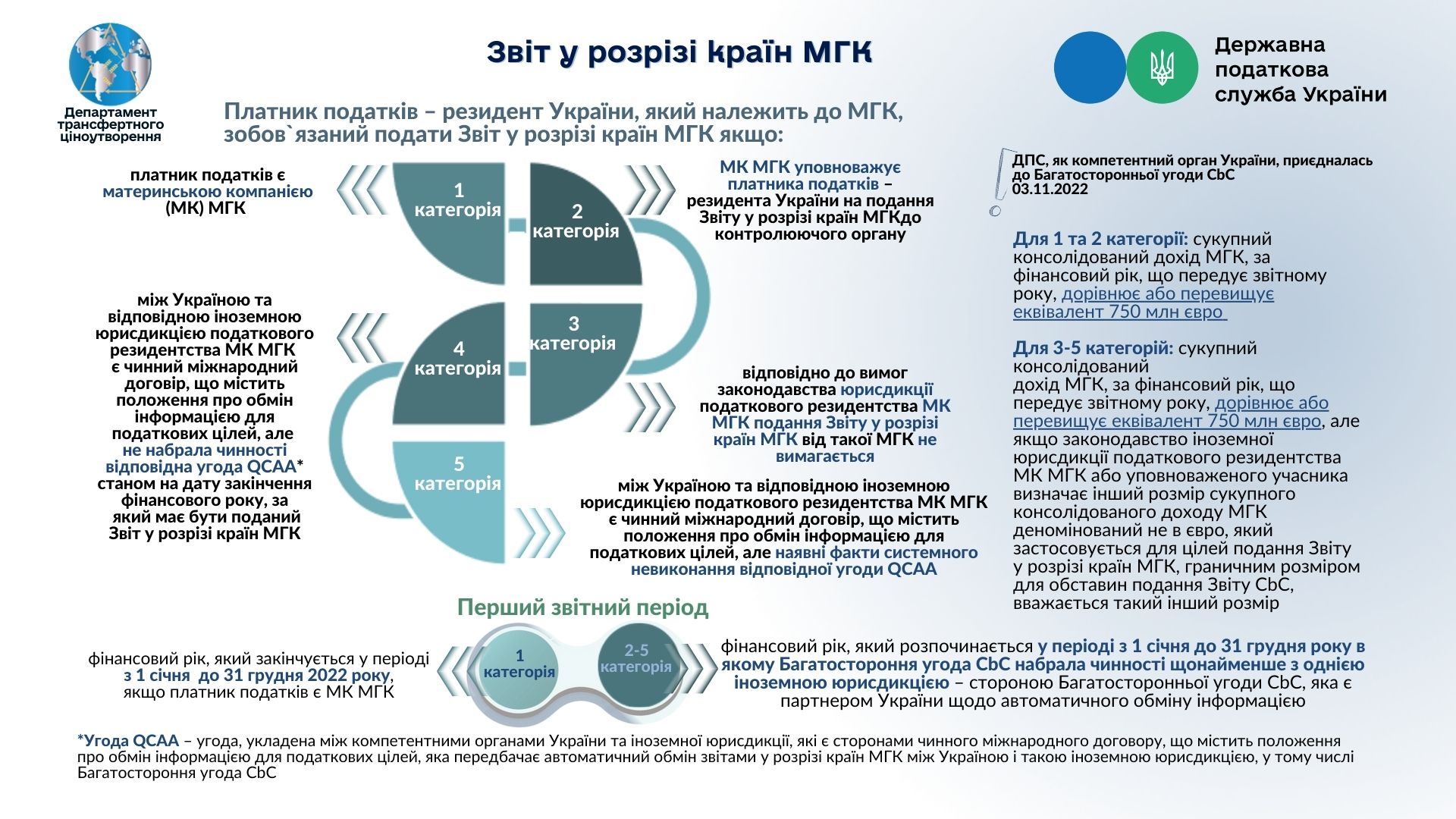

To the attention of participants of international groups of companies: Law of Ukraine No. 2970-IX as of 20.03.2023 "On amendments to the Tax Code of Ukraine and other legislative acts of Ukraine regarding implementation of the international standard of automatic information exchange on financial accounts" (hereinafter - Law No. 2970-IX) in accordance with recommendations of the Organization for Economic Cooperation and Development (https://www.oecd-ilibrary.org/taxation/country-by-country-reporting-compilation-of-2021-peer-review-reports_73dc97a6-en) introduced changes to legislation on submission of a report by country of the international group of companies (hereinafter - Report by country of the international group of companies).

In particular, Law No. 2970-IX expanded definition of the international groups of companies by referring to international groups of companies legal entities or entities without the legal entity’s status that conduct business activity through permanent representative offices in another jurisdiction (state/territory) (Sub-paragraph 14.1.1133 Paragraph 14.1 Article 14 Section I of the Tax Code of Ukraine (hereinafter - TCU)).

Changes also apply to the annual threshold value of the group's consolidated income, which will henceforth be equal to or exceed the equivalent of 750 million Euros (Clause 2 of Sub-paragraph 39.4.10 Paragraph 39.4 Article 39 Section I of the TCU).

Regarding submission of Report by country of the international group of companies, according to the updated edition, Report by country of the international group of companies is submitted in the presence of one of the following circumstances (Clauses 3 – 7 of Sub-paragraph 39.4.10 Paragraph 39.4 Article 39, Section I of the TCU):

- taxpayer is a parent company of international groups of companies;

- parent company of international groups of companies authorizes the taxpayer to submit Report by country of the international group of companies;

- legislation of the jurisdiction of the parent’s company tax residence, which does not require submission of Report by country of the international group of companies;

- between Ukraine and the corresponding foreign jurisdiction of the parent’s company tax residency of the international groups of companies, there is a valid international agreement containing provisions on the information exchange for tax purposes, but the corresponding QCAA agreement has not entered into force (Sub-paragraph 14.1.103 Paragraph 14.1 Article 14 Section I of the TCU) as of the date an end of financial year for which Report by country of the international group of companies should be submitted;

- between Ukraine and the corresponding foreign jurisdiction of the parent’ company tax residency of the international groups of companies, there is international agreement in force containing provisions on the information exchange for tax purposes, but there are facts of systematic non-fulfillment of relevant QCAA agreement.

At the same time, for residents of Ukraine – parent companies of the international group of companies, which are obliged to submit Report by country of the international group of companies, the first reporting period is financial year, which ends in a period from January 1 to December 31, 2022 (Clause 5 of Paragraph 53 Sub-section 10 Section XX "Transitional Provisions" of the TCU). That is, deadline for submitting Report by country of the international group of companies for parent companies is 31.12.2023.

For the rest of the taxpayers, the first reporting period is financial year, which begins in a period from January 1 to December 31 of year in which the Multilateral Competent Authority Agreement on the Exchange of Country-by-Country Country Reports) entered into force with at least one foreign jurisdiction (Clause 6 of Paragraph 53 Sub-section 10 Section XX "Transitional Provisions" of the TCU).

In addition, according to the new version of the TCU, only those taxpayers who are participants in respective international groups of companies and carried out controlled operations in the reporting year must submit a Notification on participation in the international groups of companies (by October 1 of year following the reporting year). This rule comes into force for reporting periods from 01.01.2022 (Clause 2 of Sub-paragraph 39.4.2 Paragraph 39.4 Article 39.4 Section I of the TCU and Clause 4 of Paragraph 53 Sub-section 10 Section XX "Transitional provisions" of the TCU).

Also, Law No. 2970-IX clarifies definition of inaccurate information contained in the Notification on participation in the international groups of companies. Namely: this is information that affected correctness of identification of each of participants of the international groups of companies, jurisdiction (state, territory) of their registration, activity, tax residency and jurisdiction of submitting Report by country of the international group of companies (Sub-paragraph 39.4.2.2 of Sub-paragraph 39.4.2 Paragraph 39.4 Article 39.4 Section I of the TCU).

Along with this, we also draw your attention to the fact that from 01.01.2024, a fine is provided for failure to submit Clarifying Report by country of the international group of companies within 30 calendar days from the date of receipt notification of detected errors in Report from the controlling body (Clause 6 of Paragraph 120.6 Article 120 Section II of the TCU), which is ten amounts of the subsistence minimum for an able-bodied person (as of January 1 of the tax (reporting) year) for each calendar day, but no more than 1000 amounts of the subsistence minimum for an able-bodied person established by the law on January 1 of the tax (reporting) year (Clause 7 of Paragraph 120.6 Article 120 Section II of the TCU).

In general, adoption of the Law No. 2970-IX and introduction of relevant amendments to the TCU ensures Ukraine's proper fulfillment of international obligations regarding the information exchange for tax purposes.