Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

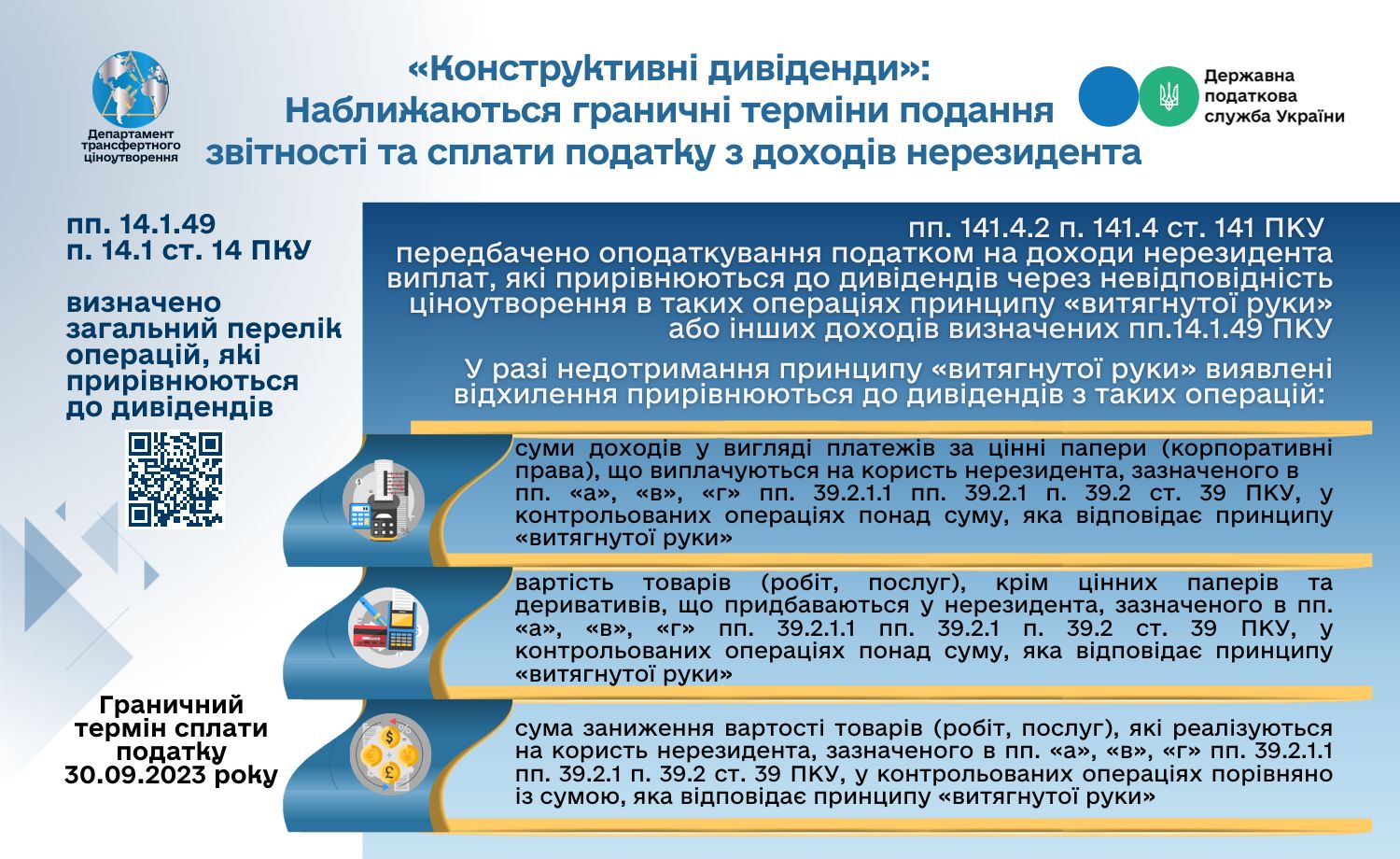

State Tax Service reminds of the approaching period of reporting and payment of taxes on income of non-residents, which are equivalent to dividends (hereinafter – "constructive dividends").

List of operations, which are equated to dividends, is given in Sub-paragraph 14.1.49 Paragraph 14.1 Article 14 of the Tax Code of Ukraine (hereinafter – Code).

At the same time, we draw attention to requirement of Sub-paragraph 141.4.2 Paragraph 141.4 Article 141 of the Code regarding taxation of non-resident income tax payments, which are equated to dividends due to the inconsistency of pricing in such operations of the "arm's length" principle.

That is, in case of non-observance of the "arm's length" principle, detected deviations are equated to dividends from the following operations:

- amounts of income in the form of payments for securities (corporate rights) paid in favor of non-resident specified in Sub-paragraphs "a", "c", "d" of Sub-paragraph 39.2.1.1 of Sub-paragraph 39.2.1 Paragraph 39.2 Article 39 of the Code, in controlled operations over amount that corresponds to the "arm's length" principle;

- cost of products (works, services), except for securities and derivatives, purchased from non-resident, specified in Sub-paragraphs "a", "c", "d" of Sub-paragraph 39.2.1.1 of Sub-paragraph 39.2.1 Paragraph 39.2 Article 39 of the Code, in controlled operations over amount that corresponds to the "arm's length" principle;

- underestimation amount of the product cost (works, services) that are sold for the non-resident’s benefit specified in Sub-paragraphs "a", "c", "d" of Sub-paragraph 39.2.1.1 of Sub-paragraph 39.2.1 Paragraph 39.2 Article 39 of the Code, in controlled operations compared to amount that corresponds to the "arm's length" principle.

From 01.01.2021, the specified incomes are taxed at the 15% rate, unless otherwise is stipulated by international agreements, or according to formula defined in Sub-paragraph 141.4.2 Paragraph 141.4 Article 141 of the Code.

Deadline for payment of tax on the income of non-residents ("constructive dividends") for adjustments of controlled operations in 2022 is 30.09.2023.

Please note the need to declare such payments by submitting annex to tax invoice to the corporate income tax declaration for three quarters of 2023 and/or for 2023. Liabilities are reflected in the income tax declaration of the reporting period in which they are paid to the budget. At the same time, it is necessary to take into account timeliness of tax payment, in particular, in case of violation of the payment deadline, it is necessary to reflect and pay fines and penalties.

Regardless of the fact of exemption from taxation, according to international agreements, taxation object is reflected in annex to invoice to the income tax declaration.

Mechanism of application of relevant international agreements is disclosed in detail in the general tax consultation of the Ministry of Finance of Ukraine № 480 as of 20.08.2021 regarding taxation issues of non-resident incomes, which are equated to dividends.

In addition, generalized information on the "constructive dividends", in particular, determination of tax base, payment terms, principles of application of provisions of international agreements, can be found at the link.