Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

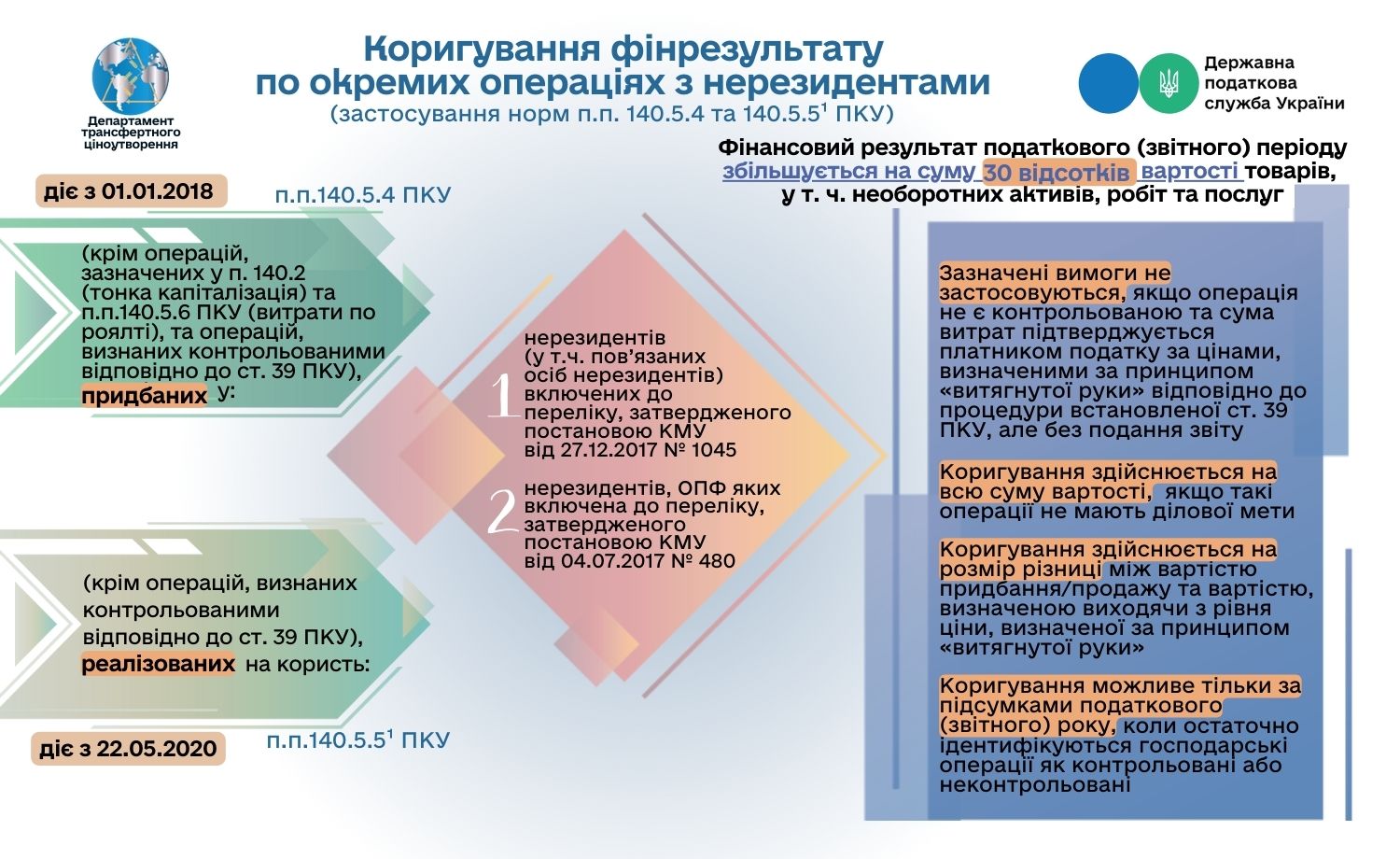

Adjustment of financial result before taxation on operations related to the purchase/sale of products, works and services carried out with certain categories of non-residents is carried out according to provisions of Sub-paragraphs 140.5.4 and 140.5.51 of Paragraph 140.5 Article 140 of the Tax Code of Ukraine (hereinafter – Code).

According to the norm of Sub-paragraph 140.5.4 Paragraph 140.5 Article 140 of the Code, financial result of the tax (reporting) period is increased by 30% of the product cost, including non-current assets (except for assets with right of use under lease agreements), works and services (except for operations specified in Paragraph 140.2 and Sub-paragraph 140.5.6 of Paragraph 140.5 Article 140 of the Code, and operations recognized as controlled according to Article 39 of the Code) purchased from:

- non-residents (including non-resident related individuals) registered in states (territories) included in the list of states (territories) approved by the Cabinet of Ministers of Ukraine according to Sub-paragraphs 39.2.1.2 and 39.2.1 of Paragraph 39.2 Article39 of the Code (Resolution of the Cabinet of Ministers of Ukraine № 1045 as of 27.12.2017);

- non-residents, whose organizational and legal form is included in the list approved by the Cabinet of Ministers of Ukraine according to Sub-paragraph "d" of Sub-paragraph 39.2.1.1 of Sub-paragraph 39.2.1 Paragraph 39.2 Article 39 of the Code, who do not pay income tax (corporate tax), including tax on income received outside the registration state of such non-residents, and/or are not tax residents of the state in which they are registered as legal entities (Resolution of the Cabinet of Ministers of Ukraine № 480 as of 04.07.2017).

Sub-paragraph 140.5.51 Paragraph 140.5 Article 140 of the Code provides that similar adjustments are made upon the product sale, including non-current assets, works and services (except for operations recognized as controlled according to Article 39 of the Code), in favor of non-residents of the above specified categories of jurisdictions (Clauses 2 and 3 of Sub-paragraph 140.5.51 Paragraph 140.5 Article 140 of the Code).

However, these requirements do not apply if operation is not controlled and amount of such expenses is confirmed by the taxpayer at prices determined according to the "arm’s length" principle according to procedure established by Article 39 of the Code, but without submission of report.

In addition, it is provided for that:

if the purchase price exceeds price determined according to the "arm’s length" principle according to procedure established by Article 39 of the Code, adjustment of financial result before taxation is carried out in the amount of difference between the purchase price and cost determined based on the price level of determined according to the "arm's length" principle;

if the sales price is lower than price determined according to the "arm's length" principle established by Article 39 of the Code, adjustment of financial result before taxation is carried out in the amount of difference between the cost determined on the basis of the price level determined according to the "arm's length" principle and the sales price.

Therefore, in case of price exceeding in case of acquisition or price undercutting upon the sale of products, works and services, specified in Sub-paragraphs 140.5.4 and 140.5.51 Paragraph 140.5 Article 140 of the Code, comparing to prices determined according to the "arm's length" principle, the taxpayer has a right to make adjustment according to Sub-paragraph 39.5.4 Paragraph 39.5 Article 39 of the Code, or such adjustment may be made to median of the price range (profitability) on the basis of review made by the controlling body.

Herewith, adjustment is made to the amount of difference between the actual cost of purchase or sale of products (works and services) and cost determined based on the price level determined according to the "arm's length" principle, and such adjustment may be less than 30% of the product cost, in including non-current assets, works and services purchased (realized) in relevant operations, and more.

Financial result before taxation is increased by the entire amount of the product cost, including non-current assets, works and services specified in Sub-paragraphs 140.5.4 and 140.5.51 Paragraph 140.5 Article 140 of the Code, both purchased and implemented for the non-residents’ benefit, in the above specified categories, if such operations do not have business purpose.

It should be noted that adjustment (increase) of financial result before taxation is possible only based on results of the tax (reporting) year, when business operations are finally identified as controlled or uncontrolled, in compliance with requirements of Sub-paragraphs 39.2.1.7 and 39.2.1 Paragraph 39.2 Article 39 of the Code.

In addition, for purposes of substantiating amount of expenses (income) for operations provided for in Sub-paragraphs 140.5.4 and 140.5.51 Paragraph 140.5 Article 140 of the Code, the taxpayer must document as a set of documents or single document compiled in an arbitrary form, information, specified in Sub-paragraph39.4.6 Paragraph 39.4 Article 39 of the Code, to the extent necessary for assessment by the taxpayer and controlling body of conformity of the price level or profitability indicator of relevant operation (operations) with the "arm's length" principle. Amount of information specified in such documentation can be considered sufficient if the taxpayer has properly substantiated the price level or profitability indicator of relevant operation (operations) using the most appropriate method, determined in Sub-paragraph 39.3.1 Paragraph 39.3 Article 39 of the Code.

Justification that amount of expenses (income) is confirmed at prices determined according to the "arm's length" principle according to procedure established by Article 39 of the Code, provided by the payer at the request of controlling body during documentary audit for the reporting period, based on results of which the taxpayer made a decision not to increase financial result, or at the request of controlling body according to Paragraph 73.3 Article 73 of the Code.

Additionally please note that the specified issues are covered in the General Tax Consultation on the application of certain provisions of Article 39 of the Tax Code of Ukraine, including adjustment of financial result before taxation on the basis of Sub-paragraph 140.5.4, 140.5.51 and 140.5.6 of Paragraph 140.5 Article 140 of the Code, which was approved by Order of the Ministry of Finance of Ukraine № 266 as of 14.05.2021.