Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

State Tax Service informs that period for paying taxes on non-residents' income equivalent to dividends (hereinafter – "constructive dividends"), including adjustments to transfer pricing for the reporting year 2022 ended on October 1, 2023.

According to the Tax Code of Ukraine (hereinafter – Code), list of operations equated to dividends for taxation purposes is given in Sub-paragraph 14.1.49 of Paragraph 14.1 Article 14 of the Code.

Sub- paragraph 141.4.2 of Paragraph 141.4 Article 141 of the Code defines requirement for taxation of "constructive dividends" due to the pricing inconsistencies in such arm's length operations.

That is, in case of non-compliance of the "arm's length" principle, detected deviations are equated to dividends from the following operations:

- amounts of income in the form of payments for securities (corporate rights) paid in favor of non-resident specified in Sub- paragraphs "a", "c", "d" of Sub-paragraph 39.2.1.1 Sub-paragraph 39.2.1 Paragraph 39.2 Article 39 of the Code, in controlled operations over amount that corresponds to the "arm's length" principle;

- cost of products (works, services), except for securities and derivatives purchased from non-resident, specified in Sub- paragraphs "a", "c", "d" of Sub-paragraph 39.2.1.1 Sub-paragraph 39.2.1 Paragraph 39.2 Article 39 of the Code, in controlled operations over amount that corresponds to the "arm's length" principle;

- amount of underestimation of the cost of products (works, services) sold to non-resident specified in Sub- paragraphs "a", "c", "d" of Sub-paragraph 39.2.1.1 Sub-paragraph 39.2.1 Paragraph 39.2 Article 39 of the Code, in controlled operations compared to amount of the arm's length principle.

Also, operations specified in Clause 7 of Sub-paragraph 14.1.49 Paragraph 14.1 Article 14 of the Code, namely, payment in monetary or non-monetary form made by a legal entity in favor of its founder and/or participant – non-resident of Ukraine in connection with a decrease in the authorized capital, purchase by the legal entity of corporate rights in its own authorized capital, outing of participant from the business partnership or another similar operation between the legal entity and its participant in amount that leads to a decrease in the legal entity’s undistributed profit.

Therefore, the specified incomes are taxed at the 15% rate, unless otherwise provided by international agreements or according to formula specified in Sub-paragraph 141.4.2 of Paragraph 141.4 Article 141 of the Code.

Mechanism of application of relevant international agreements is disclosed in detail in general tax consultation № 480 of the Ministry of Finance of Ukraine on taxation of non-residents' income equivalent to dividends as of 20.08.2021.

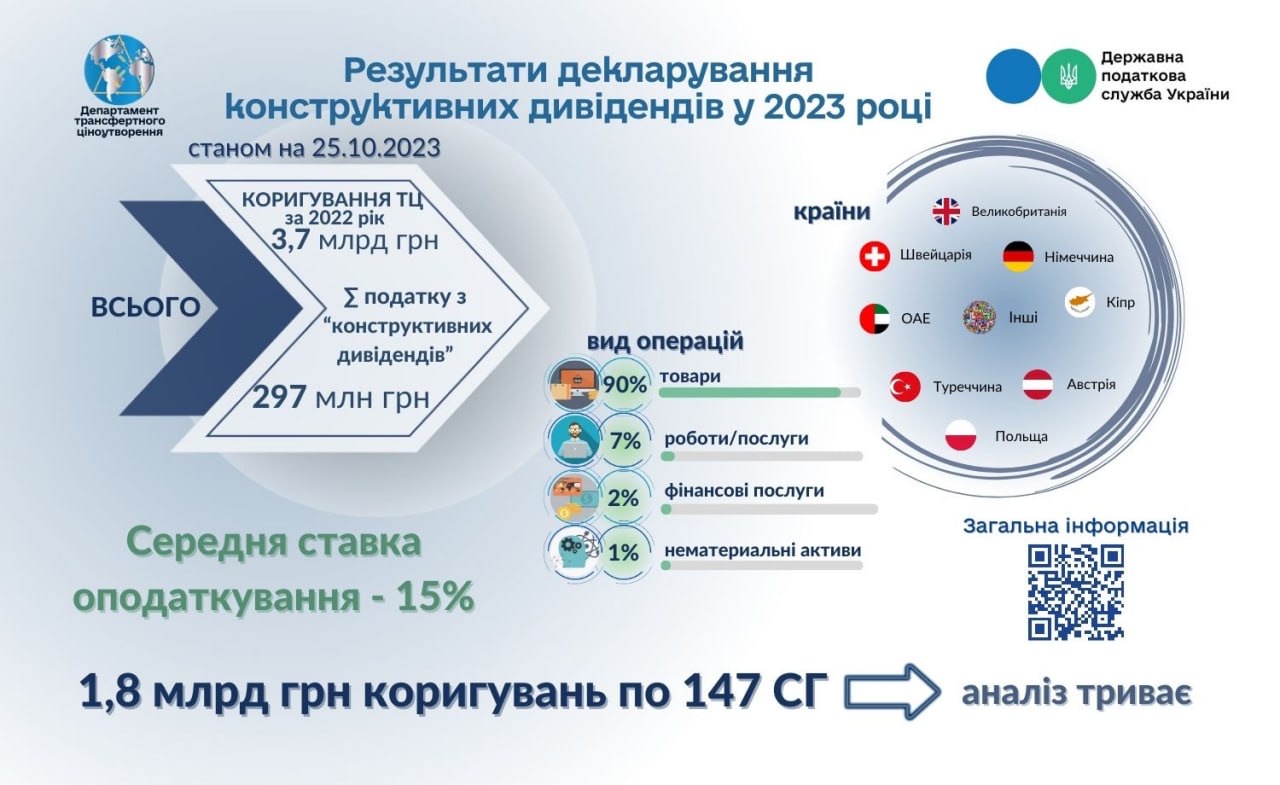

Transfer pricing adjustments were made in the amount of 3.7 billion UAH in 2023, which are equivalent to "constructive dividends". Repatriation tax in the amount of 297 million UAH has been paid as of October 1, 2023.

Processing of adjustments for 147 business entities in the amount of 1.8 billion UAH for which the repatriation tax was not paid is ongoing.

Currently, there is an ongoing campaign to declare paid "constructive dividends", due to the fact that liabilities are reflected in the income tax declaration of accounting period in which they were paid to the budget.

Therefore, please pay attention to the need to declare such payments by submitting annex Tax Invoice to the corporate income tax declaration for 9 months of 2023 and the cumulative total for 2023.

Reminder! Sub- paragraph 69.38 of Paragraph 69 Sub-section 10 Section XX “Transitional provisions” of the Code stipulates that temporarily for a period from August 1, 2023 until termination or abolition of the martial law on the territory of Ukraine, introduced by Decree № 64/2022 of the President of Ukraine "On introduction of the martial law in Ukraine" as of 24.02.2022, approved by the Law of Ukraine № 2102-IX "On approval of Decree of the President of Ukraine "On introduction of the martial law in Ukraine"" as of 24.02.2022, in case of the taxpayer’s self-correction, according to procedure, requirements and restrictions specified in Article 50 of this Code, errors that led to understatement of tax liability, such taxpayer is exempted from calculation and payment of financial sanctions and penalty provided for in Paragraph 50.1 Article 50 of this Code.