Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

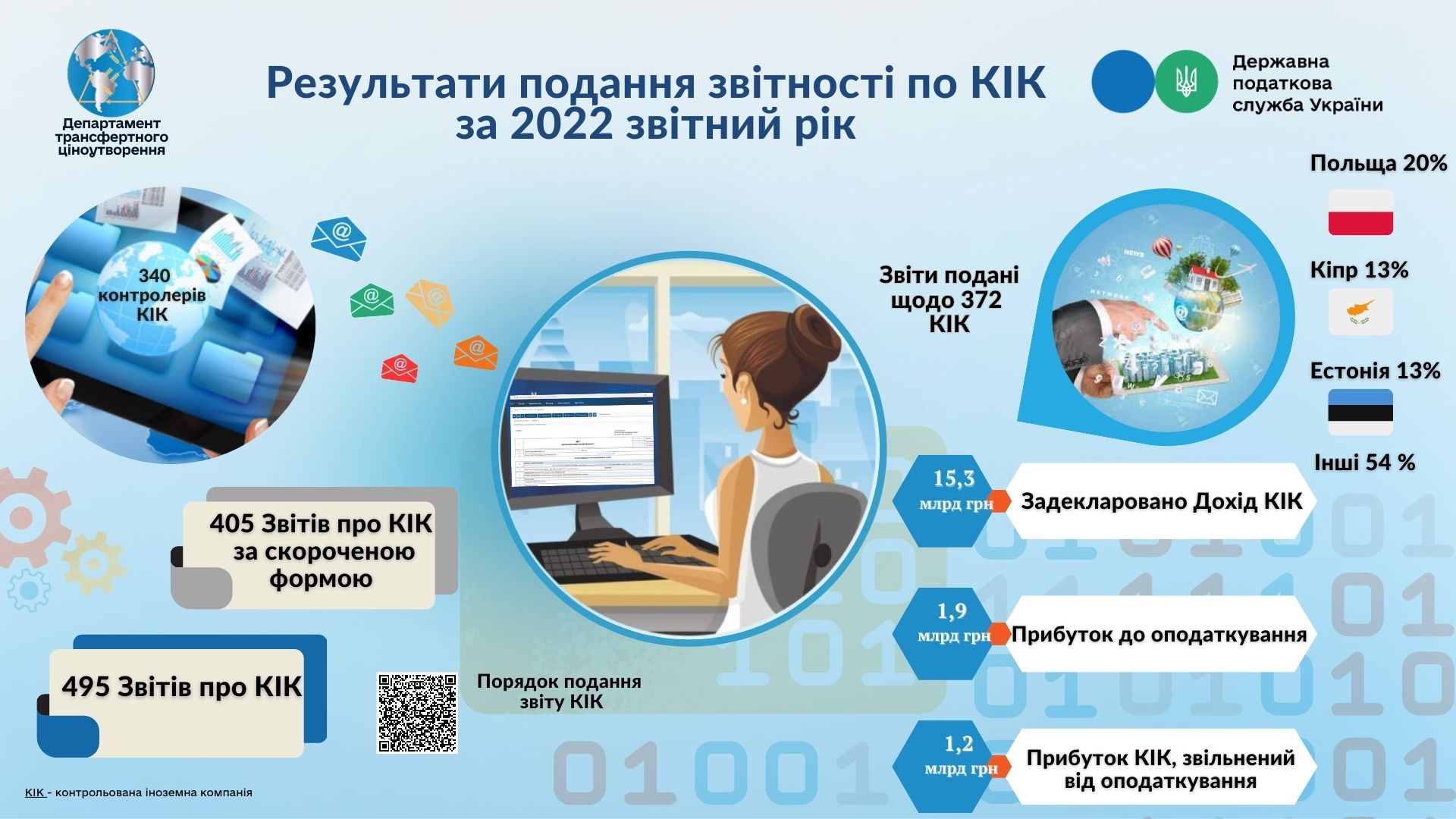

State Tax Service of Ukraine informs that campaign for submission by controlling persons of Reports on controlled foreign companies for reporting periods 2022 and 2023 is currently ongoing.

495 Reports on controlled foreign companies and 405 Reports on controlled foreign companies in the abbreviated form were received during 2023.

For tax control purposes on taxation of profit of controlled foreign companies, accounting (tax) period is a calendar year or other accounting period of controlled foreign companies ending within a calendar year.

First reporting (tax) year is 2022 (if reporting year does not correspond to a calendar year – reporting period starting in 2022).

Reminder! Report on controlled foreign companies must be submitted simultaneously with submission of annual property and income declaration (for individuals) or corporate income tax declaration (for legal entities):

- until May 1, 2024 for individuals;

- until March 1, 2024 for legal entities.

To the report on controlled foreign companies duly certified copies of financial reporting of controlled foreign companies must be attached, which confirm amount of profit of controlled foreign companies for the reporting (tax) year.

Sub-paragraph 392.5.2 Paragraph 392.5 Article 392 of the Tax Code of Ukraine (hereinafter – Code) stipulates that if deadline for preparing financial reporting in relevant foreign jurisdiction is later than deadline for submitting annual property and income declaration or corporate income tax declaration, such copies of financial reporting on controlled foreign company is submitted together with annual property and income declaration or corporate income tax declaration for the next reporting (tax) period.

Herewith, Report on controlled foreign companies contains all necessary information on the results of activities of controlled foreign companies for relevant reporting period (according to accounting data and/or interim financial reporting).

Also, if such person does not have opportunity to ensure the preparation of financial reporting on controlled foreign company and/or calculation of adjusted profit of controlled foreign company before deadline for submitting annual property and income declaration or corporate income tax declaration, such person submits report on controlled foreign company in the abbreviated form, which contains only information provided by Sub-paragraphs "a" - "c" of Sub-paragraph 392.5.2 Paragraph 392.5 Article 392 of the Code.

In case of submission of Report on controlled foreign company in the abbreviated form, the controlling person is obliged to submit full Report by the end of calendar year following the reporting (tax) year.

It must be remembered that Report on controlled foreign company is submitted for each controlled foreign company separately and exclusively in the electronic form.

At the same time, Paragraph 120.7 Article 120 of the Code establishes financial responsibility for tax violation, in particular:

non-submission of report on controlled foreign company entails imposition of a fine in the amount of 100 amounts of subsistence minimum for able-bodied person on January 1 of the tax period (302 800 UAH in 2024);

untimely submission by the controlling person of report on controlled foreign company entails imposition of a fine in the amount of 1 amount of subsistence minimum for able-bodied person established by the law on January 1 of tax year for each calendar day of non-submission, but not more than 50 amounts of subsistence minimum for able-bodied person established by the law on January 1 of the tax year (up to 151 400 UAH in 2024).

At the same time, Sub-paragraph 54 Sub-section 10 Section XX of the Code establishes that:

Financial sanctions and penalties for violating requirements of Article 392 of the Code determining and calculating profit of the controlled foreign company are not applied for results of the reporting (tax) years 2022 – 2023;

according to results of reporting (tax) years 2022 – 2023, administrative and criminal liability for any violations related to application of provisions of Article 392of the Code are not applied to the taxpayer, officials.