Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

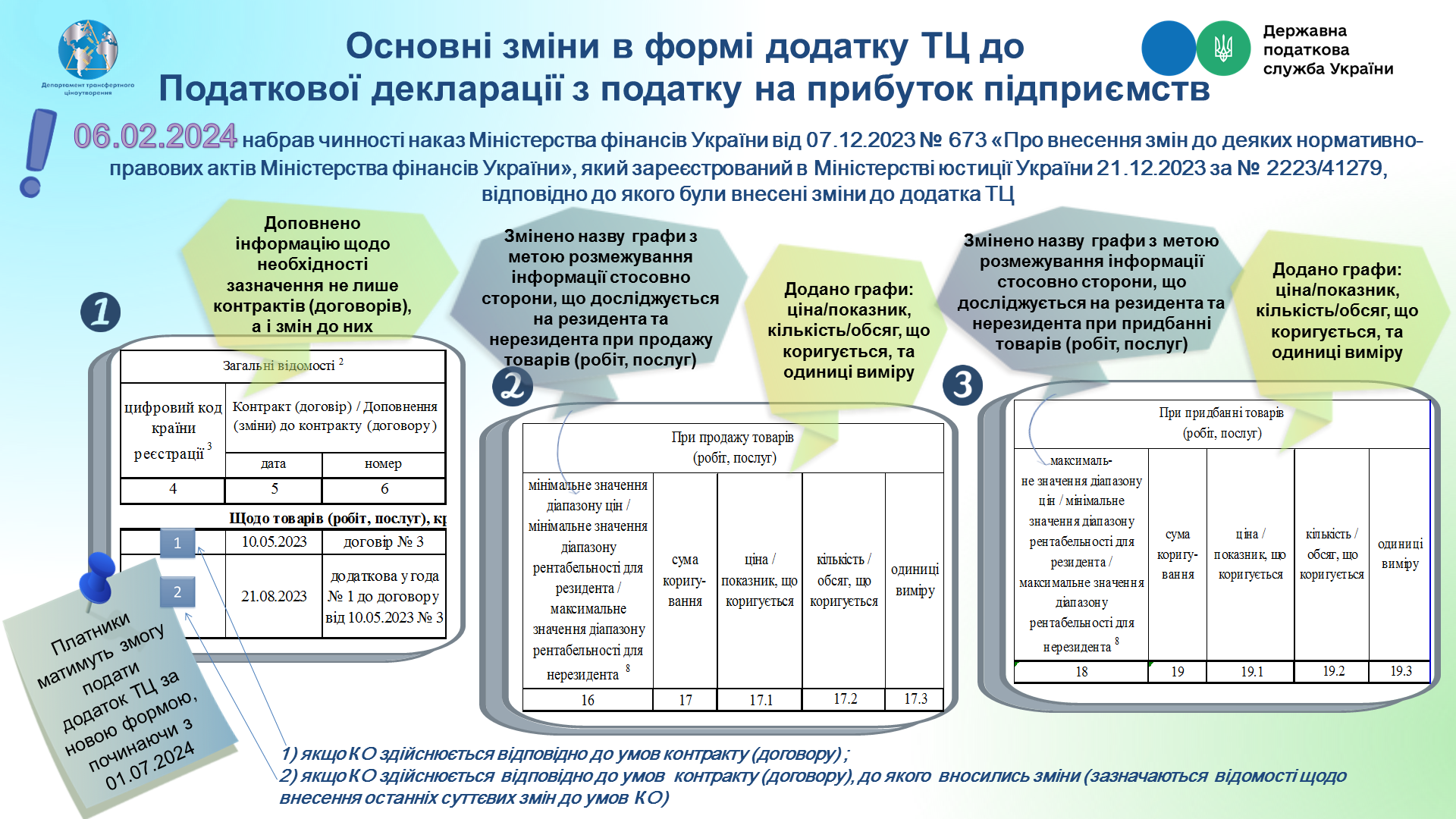

State Tax Service of Ukraine informs that Order of the Ministry of Finance of Ukraine № 673 as of 07.12.2023 "On amendments to certain regulatory acts of the Ministry of Finance of Ukraine", registered in the Ministry of Justice of Ukraine on 21.12.2023 under № 2223/41279, entered into force on 06.02.2024 (hereinafter – Order № 673) (with changes).

This Order, with aim of improving control over compliance with conditions of controlled operations with the "arm's length" principle, made changes to form of the Transfer Pricing Addendum (Independent price adjustment of controlled operation and amount of the taxpayer’s tax liability) to the Corporate income tax declaration (hereinafter – Transfer Pricing Addendum), approved by Order of the Ministry of Finance of Ukraine № 897 as of 20.10.2015, registered in the Ministry of Justice of Ukraine on 11.11.2015 under № 1415/27860 (with changes).

Above specified was posted on web portal of the State Tax Service in section: Home/Press Center/News (link – https://tax.gov.ua/en/mass-media/news/760878.html).

It is worth paying attention to the following main changes to the Transfer Pricing Addendum, namely:

- columns 5 and 6 – information was added on the need to indicate not only contracts (agreements), but also changes to them, which confirm agreement by the parties of essential contract terms, in particular, characteristics of the product price, volume, supply terms, payment and parties’ responsibility of the controlled operation (example of filling column 5 and 6 are in the infographic);

- column 16 – in order to distinguish information about the party under verification as a resident and non-resident upon the sale of products (works, services), the column’s title has been changed (minimum value of price / profitability range for resident and maximum value of profitability range for non-resident);

- column 18 – in order to distinguish information about the party under verification as a resident and non-resident upon the sale of products (works, services), the column’s title has been changed (maximum value of price range / minimum value of profitability range for resident and maximum value of profitability range for non-resident);

- new columns were added that reflect information about:

column 17.1 – prices or indicators adjusted upon the sale of products (works, services);

column 17.2 –amount or volume adjusted upon the sale of products (works, services);

column 17.3 – measurement units upon the sale of products (works, services);

column 19.1 – prices or indicator that is adjusted upon the sale of products (works, services);

column 19.2 – amount or volume that is adjusted upon the sale of products (works, services);

column 19.3 – measurement units upon the sale of products (works, services).

The updated XML scheme of the Corporate income tax declaration (with annexes) (J0100126 with a note "for developers)" is published on web portal of the State Tax Service in section: Home/Electronic reporting/For taxpayers on electronic reporting/Information and analytical support/Register of electronic forms of tax documents.

Provisions of Paragraph 46.6 Article 46 of the Tax Code of Ukraine (hereinafter – Code) stipulate that, if forms of tax reporting are changed as a result of changes in taxation rules, before definition of new forms of declarations (calculations), which enter into force for preparation of reports for tax period that follows tax period, in which their publication took place, forms of declarations (calculations) valid before such determination are valid.

In view of the above specified, applications of the Transfer Pricing Addendum submitted by taxpayers in the non-updated version of electronic formats before entry into force of Order № 673 are considered valid.

In case of submitting clarifying calculation to the Corporate income tax declaration for previous tax (reporting) year for the purpose of making independent adjustment according to Article 39 of the Code or determining tax base according to Sub-paragraph 141.91.3 Paragraph 141.91 Article 141 of the Code in case of controlled operations, if their conditions do not meet the "arm's length" principle, not later than October 1 of year following the reporting year, a fine of three percent of the amount of underpayment is not applied (Paragraph 50.1 Article 50 of the Code).

Income tax payers, in case of self-adjustment of price of the controlled operation and tax amount of payer's tax liabilities carried out according to Sub-paragraph 39.5.4 Paragraph 39.5 Article 39 of Section I of the Code, will be able to submit the Transfer Pricing Addendum in the updated form (including in the due to clarification of indicators for tax (reporting) year 2023), starting from 07.01.2024.