Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

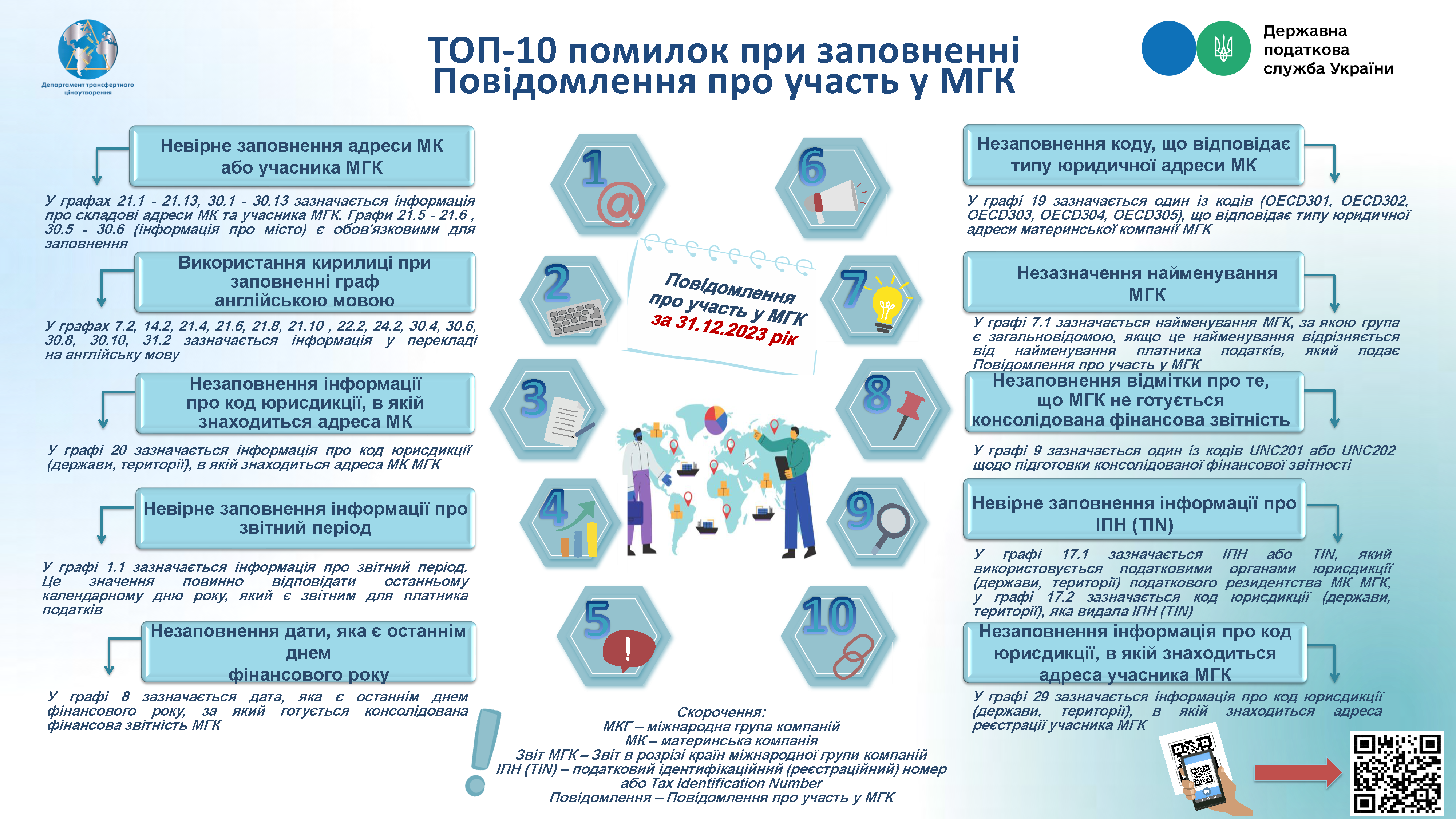

On the basis of annual monitoring of submitted Notifications on participation in the international group of companies, specialists of the State Tax Service summarized the most common taxpayers’ mistakes in the process of filling out Notification on participation in the international group of companies.

The following mistakes were included in the TOP 10 (depending on the frequency of their admission by the taxpayers):

incorrect filling of address of the parent company or member of the international group of companies – in columns 21.1 - 21.13, 30.1 - 30.13, information about components of addresses of the parent company and member of the international group of companies is indicated. Columns 21.5 - 21.6, 30.5 - 30.6 (city information) are obligatory;

use of Cyrillic alphabet filling in columns in English – in columns 7.2, 14.2, 21.4, 21.6, 21.8, 21.10, 22.2, 24.2, 30.4, 30.6, 30.8, 30.10, 31.2, information translated into English is indicated;

failure to fill in information about code of the jurisdiction in which address of the parent company is located – in column 20, enter information about code of the jurisdiction (state, territory) in which address of the parent company of the international group of companies is located;

incorrect filling out information about the reporting period – information about the reporting period is indicated in column 1.1. This value must correspond to the last calendar day of the reporting year for the taxpayer;

failure to fill in the date, which is the last day of financial year – column 8 indicates the date, which is the last day of financial year, for which the consolidated financial reporting of the international group of companies are prepared;

failure to fill in code corresponding to the type of legal address of the parent company – in column 19, one of the codes (OECD301, OECD302, OECD303, OECD304, OECD305) corresponding to the type of legal address of the parent company of the international group of companies is indicated;

failure to indicate name of the international group of companies – in column 7.1, name of the international group of companies by which the group is commonly known is indicated, if this name differs from the name of taxpayer who submits Notification on participation in the international group of companies;

failure to fill in the note that consolidated financial reporting are not prepared for the international group of companies – column 9 indicates one of the codes UNC201 or UNC202 regarding preparation of the consolidated financial reporting;

incorrect filling of information about the Individual tax number (TIN) – in column 17.1, the Individual tax number or TIN, which is used by the tax authorities of jurisdiction (state, territory) of tax residence of the parent company of the international group of companies, is indicated; code of jurisdiction (state, territory), which issued the Individual tax number (TIN) is indicated in column 17.2;

failure to fill in information about the code of jurisdiction in which address of participant of the international group of companies is located – column 29 contains information about the code of jurisdiction (state, territory) in which registration address of participant of the international group of companies is located is indicated, provided that Report by country of the international group of companies is submitted by authorized member of the international group of companies, and the total consolidated income of the international group of companies for financial year preceding reporting one is equal to or exceeds the equivalent of 750 million euros.

In order to simplify perception, specialists of the State Tax Service prepared infographic, which contains both examples of the most common mistakes in the process of filling out Notification on participation in the international group of companies, as well as specific advice on how to avoid them in the future.

It is recommended to the specified information in order to avoid errors in the process of filling out the above specified notification. Self-detection and timely correction of errors will protect taxpayers from negative consequences in the form of fines.

It should be noted that Article 120 of the Tax Code of Ukraine (hereinafter – Code) provides for the taxpayers’ responsibility for non-submission, untimely submission or provision of inaccurate information in Notification on participation in the international group of companies.

As an example, according to Paragraph 120.5 Article 120 of the Code, fine for providing inaccurate information in Notification on participation in the international group of companies is 50 times the subsistence minimum for able-bodied person, established by the law on January 1 of tax (reporting) year, in particular, for 2023 – 134 200 UAH (50 x 2,684 UAH).

In addition, fine provided for in Paragraph 120.5 Article 120 of the Code does not apply if the taxpayer has submitted Notification on participation in the international group of companies and/or a Country-by-Country Report of the international group of companies with errors that did not affect correctness of identification of the state or territory of which the taxpayer is a resident there is one or more participants in the international group of companies, and/or on correct identification of each of participants in the corresponding international group of companies, and/or on correct identification of jurisdiction of submission of Country-by-Country report of the international group of companies, and such payer corrected errors by submitting a clarifying Notification on participation in the international group of companies and/or the Country-by-Country report of the international group of companies independently or not later than 30 calendar days from the date of receipt of the controlling authority's notification of the identified errors in the Country-by-Country Report of the international group of companies.