Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

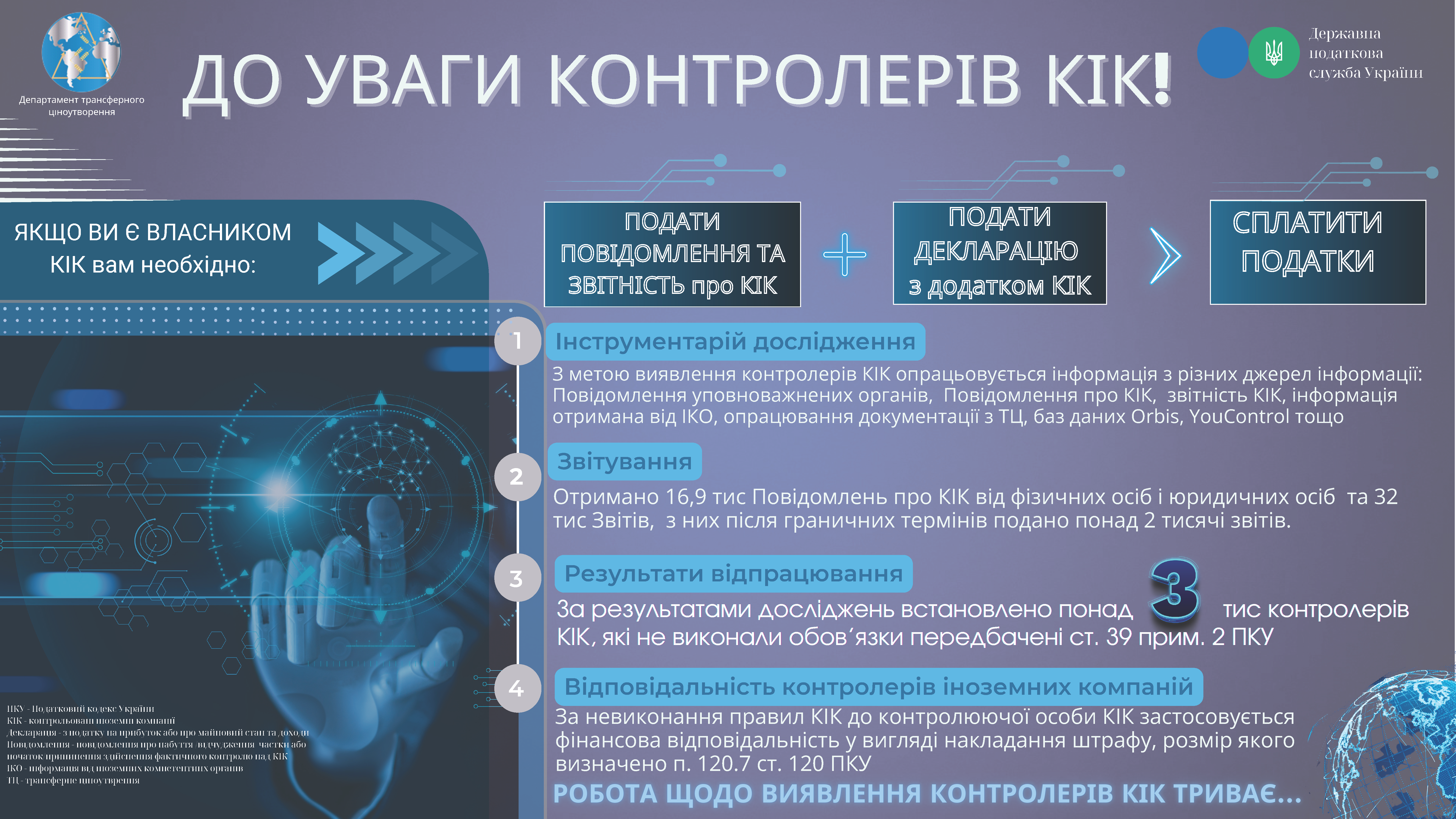

Controllers of controlled foreign companies are required to submit Notifications on controlled foreign companies, Reports on controlled foreign companies, property and income tax declarations and pay taxes from 2022.

Article 392 of the Tax Code of Ukraine (hereinafter – Code) stipulates that if resident of Ukraine (individual/legal entity) has registered legal entity in the foreign state/territory, and in some cases, entity without the legal entity’s status (for example: trusts, foundations), such legal entity (formation without the legal entity’s status) is a controlled foreign company.

For failure to comply with rules of controlled foreign companies, the controlling entity is subject to financial responsibility in the form of a fine, amount of which is determined by Paragraph 120.7 Article 120 Section II of the Code.

For a period from 01.01.2022 to 01.09.2024, the controlling authority received 16 917 Notifications on controlled foreign companies, of which 16 400 were from individuals-residents of Ukraine and 517 from legal entities-residents of Ukraine for 8 482 controlled foreign companies.

Also, 21 817 full Reports on controlled foreign companies and 10 354 Reports in the abbreviated form were received, of which more than 2 000 reports were submitted after the deadline.

However, it should be emphasized that the controlling authority, in order to identify potential controllers of controlled foreign companies, applies a comprehensive approach, which consists, in particular, of the analysis of reporting discipline (failure to submit Notifications, timeliness of submission and failure to submit reports on controlled foreign companies), completeness and reliability of information reflection in reports on controlled foreign companies; analysis of information and financial reporting indicators, audit conclusions, transfer pricing documentation, primary documents of controlled foreign companies; analysis of open sources of information, mass media, international databases, OSINT, reports from authorized bodies, processing of information received through exchange with foreign competent bodies, etc.

Such approach has already made it possible to establish more than 3 000 controllers of controlled foreign companies who failed to fulfill their obligations in a timely manner according to Article 392 Section I of the Code.

In view of the above specified, the State Tax Service of Ukraine emphasizes the need for controlling entities to comply with rules of controlled foreign companies, which are regulated by Article 392 Section I of the Code.

Work is currently ongoing to establish controllers of controlled foreign companies and the need for appropriate reporting on controlled foreign companies.