Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

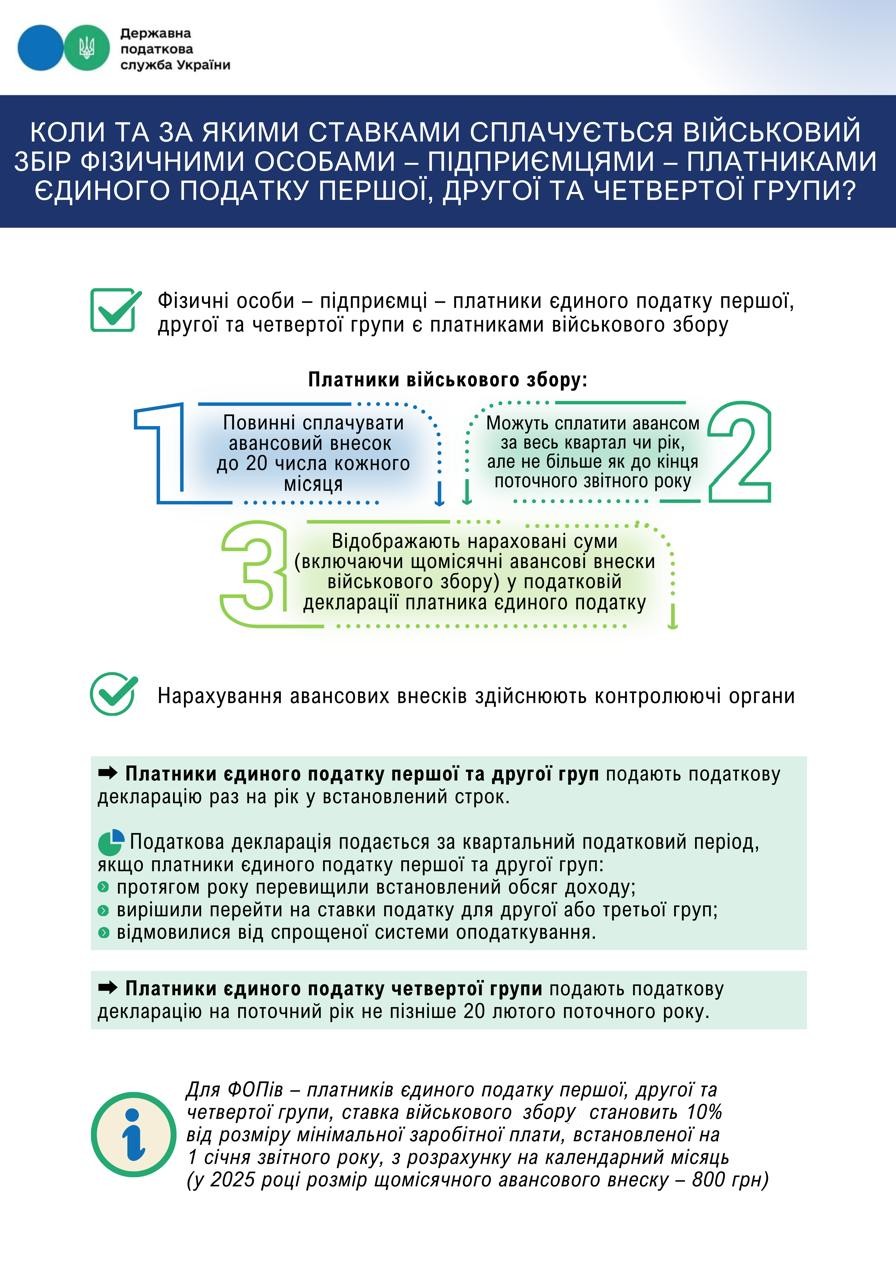

Individuals-entrepreneurs – single tax payers of Groups I, II and IV are military levy payers.

Military levy payers:

Must pay advance payment by the 20th of each month;

Can pay in advance for the entire quarter or year, but not more than until the end of current reporting year;

Reflect accrued amounts (including monthly advance military levy’s payments) in the single tax payer’s declaration.

Accrual of advance payments is carried out by controlling authorities.

Single tax payers of Groups I and II submit tax declaration once a year within the established deadline.

Tax declaration is submitted for a quarterly tax period if single tax payers of Groups I and II:

exceeded the established amount of income during a year;

decided to switch to tax rates for Groups II and III;

refused the simplified taxation system.

Single tax payers of Group IV submit tax declaration for the current year not later than February 20 of the current year.

For individuals-entrepreneurs – single tax payers of Groups I, II and IV, the military levy rate is 10% of the minimum wage established on January 1 of the reporting year, calculated per calendar month (amount of monthly advance payment is 800 UAH in 2025).