Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

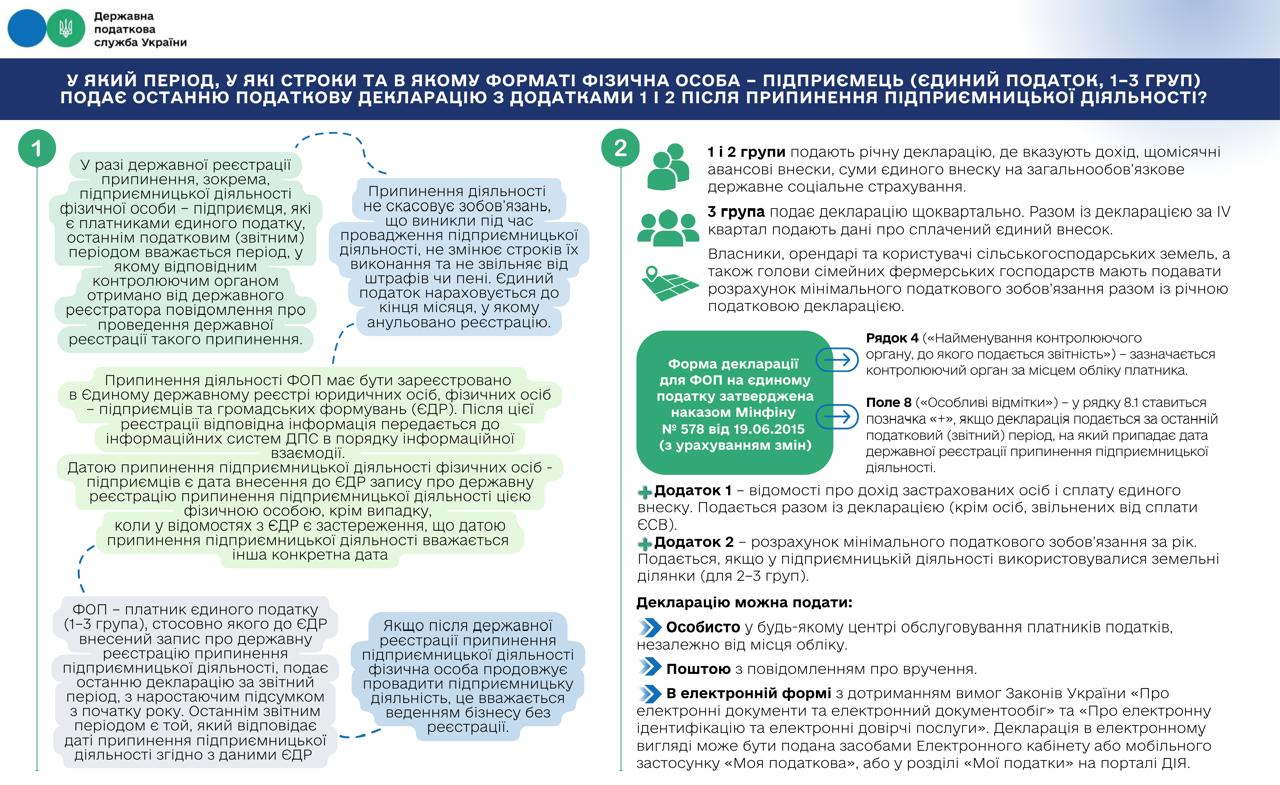

In case of state registration of termination, particularly of entrepreneurial activity of individual-entrepreneur who is the single tax payer, the last tax (reporting) period is considered to be period in which relevant controlling authority received notification from the State registrar about the state registration of such termination.

Termination of activity of individual-entrepreneur must be registered in the Unified state register of legal entities, individuals-entrepreneurs and public organizations (hereinafter – Unified state register). After this registration, relevant information is transferred to information systems of the State Tax Service in order of information interaction. Termination date of entrepreneurial activity of individuals-entrepreneurs is the date of entry in the Unified state register of record on the state registration of termination of entrepreneurial activity by this individual-entrepreneur, except for the case when information from the Unified state register contains a reservation that the termination date of entrepreneurial activity is considered to be another specific date**.

Termination of activity does not cancel obligations that arose during the conduction of entrepreneurial activity, does not change deadlines for their fulfillment and does not exempt from fines or penalties. Single tax is accrued until the end of month in which registration was canceled.

Individual-entrepreneur – single tax payer (Groups I–III), for whom record of state registration of termination of entrepreneurial activity has been entered in the Unified state register, submits the last declaration for the reporting period, with a cumulative total from the beginning of year. The last reporting period is the one that corresponds to the termination date of entrepreneurial activity according to the Unified state register.

If, after the state registration of termination of entrepreneurial activity, individual continues to conduct entrepreneurial activity, this is considered conducting business without registration.

Single tax payers:

Groups I and II submit annual declaration indicating income, monthly advance payments and amount of the single contribution to obligatory state social insurance.

Group III submits declaration quarterly. Together with declaration for the IV quarter, they submit data regarding paid single contribution.

Owners, tenants and users of agricultural land, as well as heads of family farms, must submit calculation of the minimum tax liability together with annual tax declaration.

Declaration form for individuals-entrepreneurs on the single tax was approved by Order of the Ministry of Finance № 578 as of 19.06.2015 (with changes).

Regarding filling out the Declaration:

Line 4 ("Title of the controlling authority to which report is submitted") – the controlling authority at the payer’s registration place is indicated.

Field 8 (“Special notes”) – in line 8.1, a “+” mark is indicated if the declaration is submitted for the last tax (reporting) period, which includes the date of state registration of termination of entrepreneurial activity.

The Declaration is attached with:

Annex 1 – information regarding income of insured persons and payment of single social contribution. Annex is submitted together with the declaration (except for persons exempted from paying single contribution).

Annex 2 – calculation of the minimum tax liability for a year. Annex is submitted if land plots were used in entrepreneurial activity (for Groups II–III).

The Declaration can be submitted:

1. In person at any Taxpayer Service Center, regardless of the registration place.

2. By mail with delivery notification.

3. In the electronic form in compliance with requirements of the Laws of Ukraine "On electronic documents and electronic document management" and "On electronic identification and electronic trust services". Declaration in the electronic form can be submitted using the Electronic cabinet or mobile application "My Tax Service", or in "My Taxes" section on the DIIA portal.

*Contact Center of the State Tax Service of Ukraine provides consultations to the taxpayers, clarifications regarding tax legislation and assistance in resolving tax-related questions. Total number of applications received last year reached 1 062 448.

How to contact? Hotline: 0 800 501 007 (free calls). E-mail: idd@tax.gov.ua. Personal account: Through the taxpayer’s electronic cabinet.

Working hours: Monday–Friday, from 08:00 to 18:00.

**Part 9 Article 4 of the Law of Ukraine “On State registration of legal entities, individuals-entrepreneurs and public organizations” № 755 establishes that individual-entrepreneur is deprived of the status of entrepreneur from the date of entry in the Unified state register of record on the state registration of termination of entrepreneurial activity by this individual.

Registration peculiarities of termination of entrepreneurial activity of individual-entrepreneurs under conditions of temporary restriction of access to the Unified state register are determined by Resolution of the Cabinet of Ministers of Ukraine № 1546 as of 31.12.2024 “Some matters of functioning of the Unified state register of legal entities and individuals-entrepreneurs”. Date of state registration of termination of entrepreneurial activity of individual-entrepreneur, carried out according to this Resolution, is considered to be the date of submission of relevant application.