Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

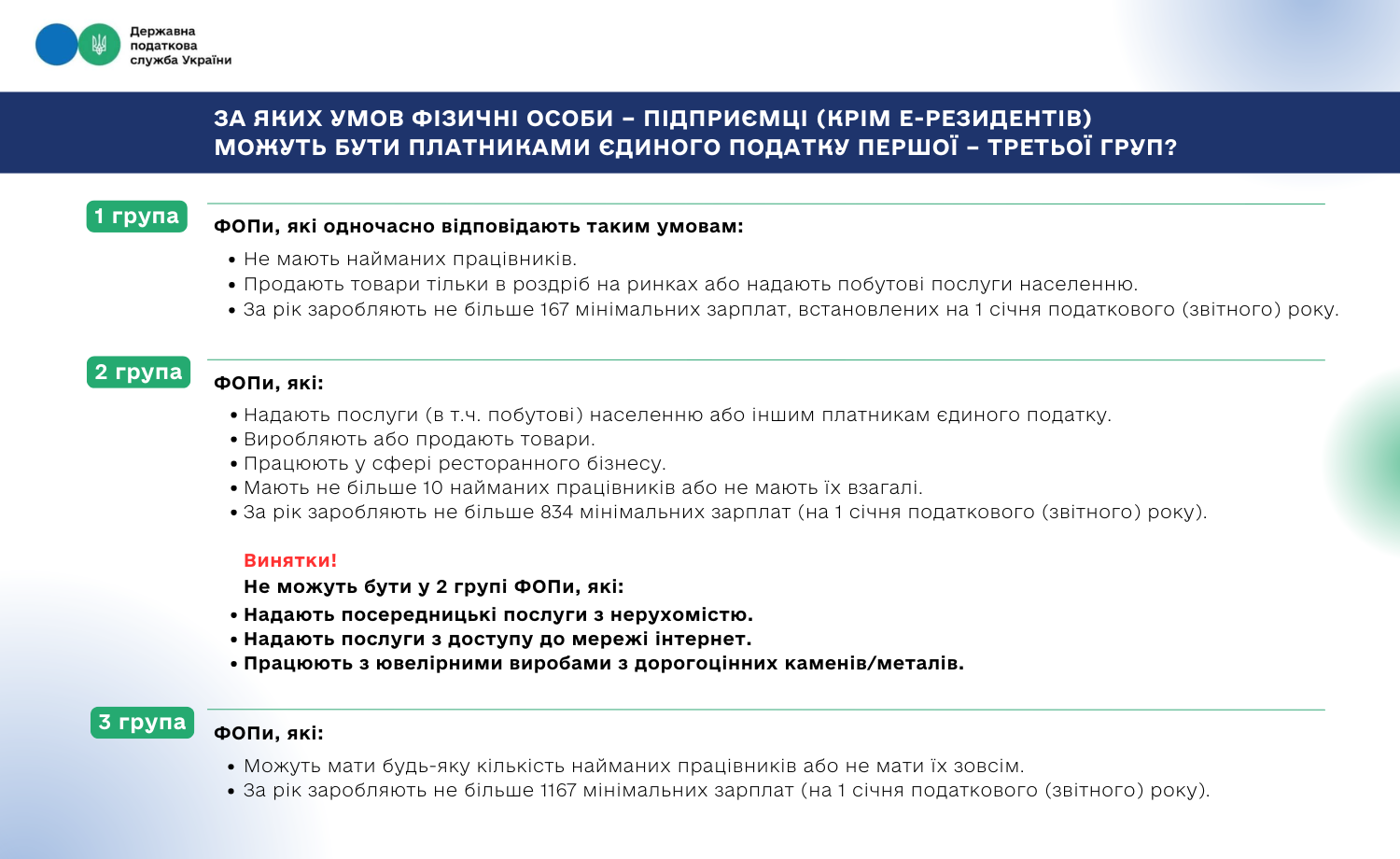

Specialists of the State Tax Service answer popular questions to the Contact Center. Taxpayers are often interested in procedure for individuals-entrepreneurs, except for the e-residents, to be on the simplified taxation system.

Answer:

Who is the single tax payer?

Group I:

- Individual-entrepreneur without hired employees;

- carry out retail product sales in markets and/or provide household services to the population;

- annual income – not more than 167 minimum wages (as of January 1 of the reporting year).

Group II:

Individual-entrepreneur who provide services (including household services) to the population or the single tax payers involved in production or product sale and work in the restaurant industry:

- number of employees – not more than 10 people at the same time or no employees at all;

- annual income – not more than 834 minimum wages (as of January 1 of the reporting year).

Exceptions: Individual-entrepreneur that provide real estate brokerage services, provide Internet access; involved in production, supply and sale of jewelry and household products made of precious metals/stones.

Group III:

- Individual-entrepreneur without restrictions on the number of employees;

- annual income – does not exceed 1 167 minimum wages (as of January 1 of the reporting year).

Who cannot be the single tax payer (Groups I – III)?

Simplified system for individuals-entrepreneurs involved in:

- gambling;

- currency exchange;

- production and sale of excisable products (with some exceptions),

- mining of minerals, precious metals and stones;

- financial intermediation (except for insurance agents and certain specialists defined by the law);

- provision of postal and telecommunications services (except for the courier services);

- sale of art objects, antiques, organization of auctions;

- organization of touring events;

- technical testing, research, audit;

- leasing of land plots of more than 0.2 hectares, residential premises of more than 400 square meters non-residential premises of more than 900 square meters.

Exceptions: banks, insurance companies, pawnshops, credit unions, other financial institutions, securities registrars, non-resident individuals, as well as payers with the tax debt (except for the bad tax debt arising from the force majeure circumstances)).

For reference: Procedure for individual-entrepreneur to stay on the simplified system is determined by Article 291 of the Tax Code of Ukraine.