Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

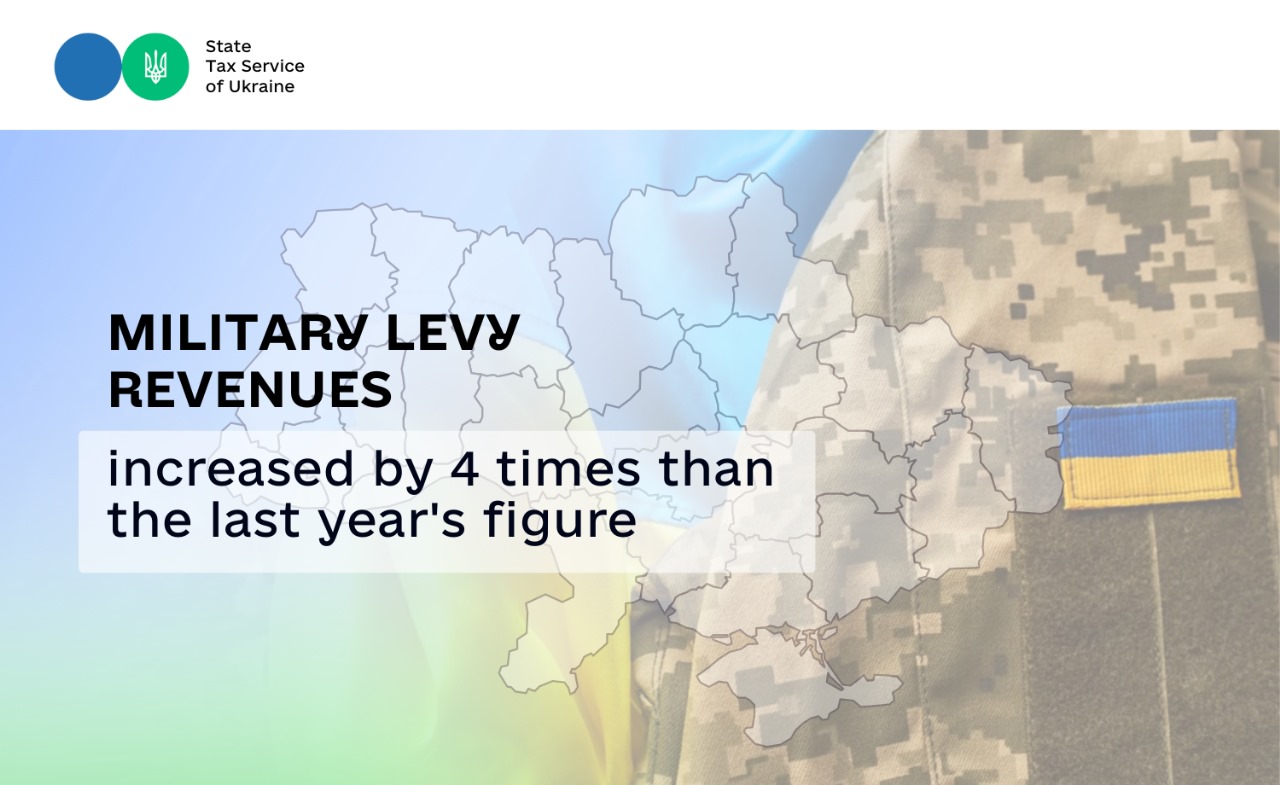

In the first 8 months of this year, the taxpayers paid almost 116.7 billion UAH of military levy to the budget. This is almost 4 times more than in the same period last year (+84.2 billion UAH).

Revenues amounted to 32.5 billion UAH in 9 months last year.

Growth is due to both increase in the military levy rate to 5% from December 1, 2024 and conscious position of the taxpayers who pay taxes on time and support our military.

The most paid:

Kyiv city – 37.7 billion UAH,

Dnipropetrovsk region – 13.2 billion UAH,

Lviv region – 9 billion UAH,

Kharkiv region – 7.4 billion UAH.

Military levy is paid by all categories of taxpayers.

Military levy rates:

Individuals-entrepreneurs of the I, II and IV groups – 10% of the minimum salary established on January 1 of the reporting year (monthly advance payment is 800 UAH in 2025).

Single tax payers of the group III (except for the e-residents) – 1% of income received quarterly.

Entrepreneurs on the general taxation system – 5% of the net annual taxable income.

For hired employees – 5% of accrued salaries.

Military servicemen and employees of the Armed Forces of Ukraine, Security Service of Ukraine, Foreign Intelligence Service of Ukraine, State Border Guard Service, State Security Service of Ukraine, State Special Communications Service, State Special Transport Service of Ukraine – 1.5% of income received in the form of cash benefits, monetary rewards and other payments made according to legislation of Ukraine (except for income exempted from military levy according to Sub-paragraph 1.7 Paragraph 16 Note 1 Sub-section 10 Section XX of the Tax Code of Ukraine).

Self-employed individuals who have been mobilized or signed a contract for military service are exempted from paying military levy for the service period. This is provided for by the Law of Ukraine № 4505-IХ as of 18.06.2025, which made changes the Tax Code of Ukraine.

Exemption is applied automatically based on data from the Unified state register of conscripts, servicemen and reservists (mobilization dates, conclusion of a contract, demobilization) from the first day of month of mobilization or conclusion of a contract, but not earlier than February 24, 2022.