Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portalT he last day in 2022 for submitting tax reporting to acquire or confirm status of the single tax payer of Group IV is 21.02.2022.

Confirmation of status of the single tax payer of Group IV for agricultural producers is annual according to requirements of Sub-paragraph 298.8.1 Paragraph 298.8 Article 298 of the Tax Code of Ukraine.

One of conditions for acquiring or confirming status of the single tax payer of Group IV is submission by agricultural producers of a complete list of tax reporting of the single tax payer of Group IV, namely:

general tax declaration of the single tax payer of Group IV;

reporting tax declaration of the single tax payer of Group IV;

information on the availability of land plots, which are an integral part of tax declaration;

calculation of share of agricultural production.

Please pay attention to peculiarities of filling in the general tax declaration of the single tax payer of Group IV.

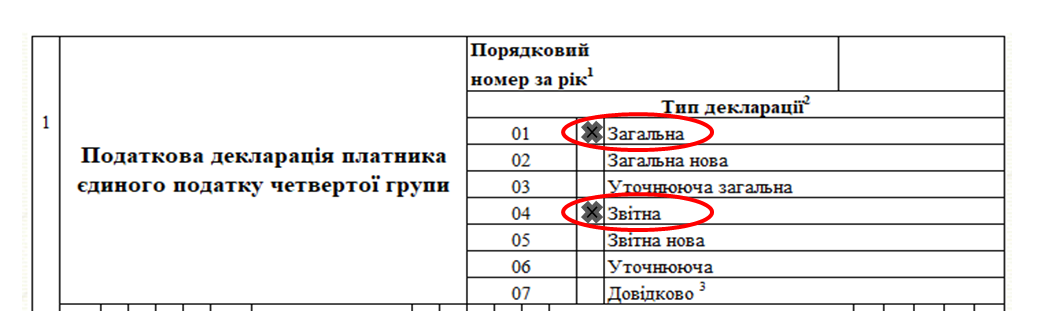

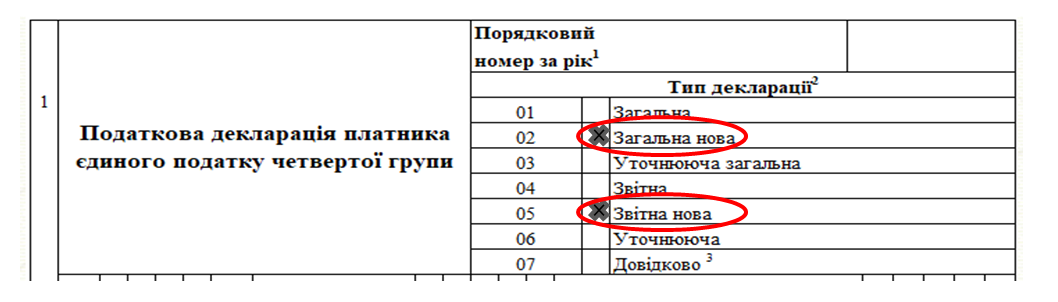

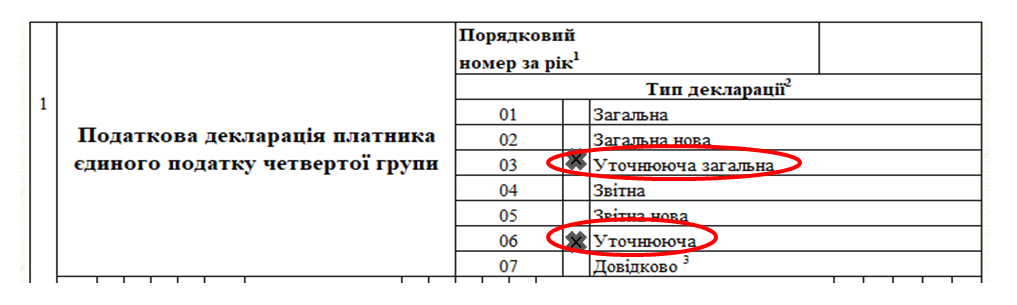

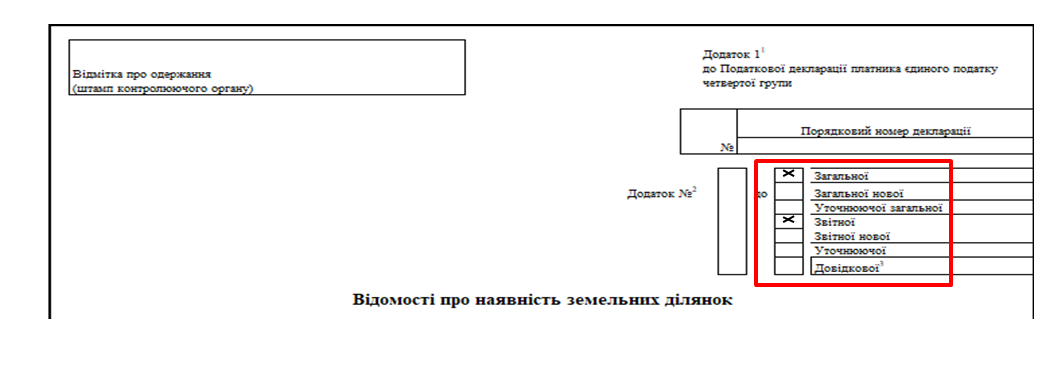

General tax declaration of the single tax payer of Group IV must contain two marks in its type: "General" and "Reporting".

If business entity submits general new or clarifying general declaration, the type of declaration must be marked accordingly:

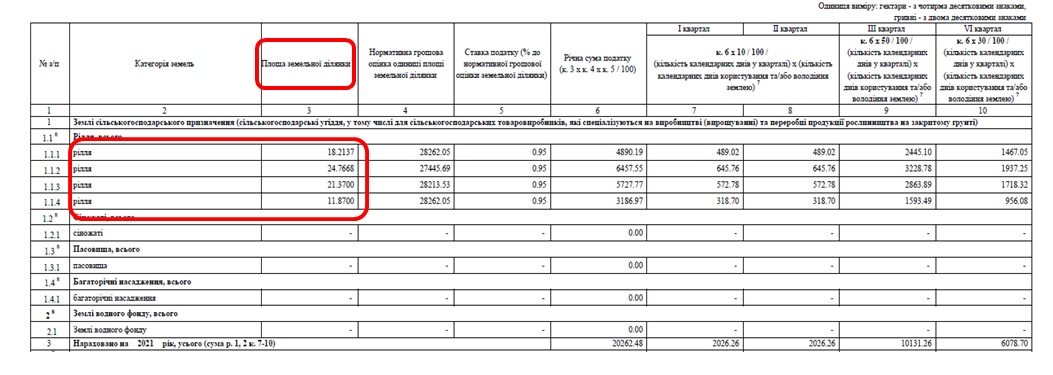

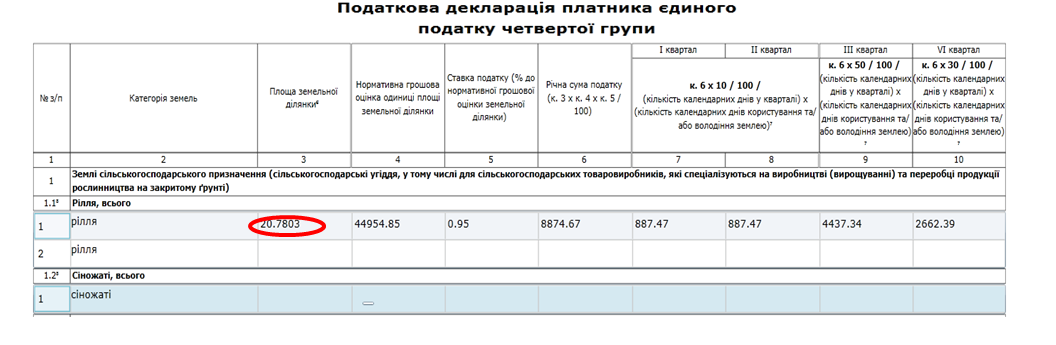

In addition, general tax declaration of the single tax payer of Group IV indicates the total area of land owned or used by agricultural producers.

General declaration is submitted to the controlling body at the main tax accounting place, which is indicated in line 7 of tax declaration’s general part.

Reporting tax declarations of the single tax payer of Group IV are submitted separately to each controlling body, whose powers include territory of the territorial community where the land plots owned or used (including on lease terms) of agricultural producer are located; line 8 of tax declaration’s general part is filled in accordingly.

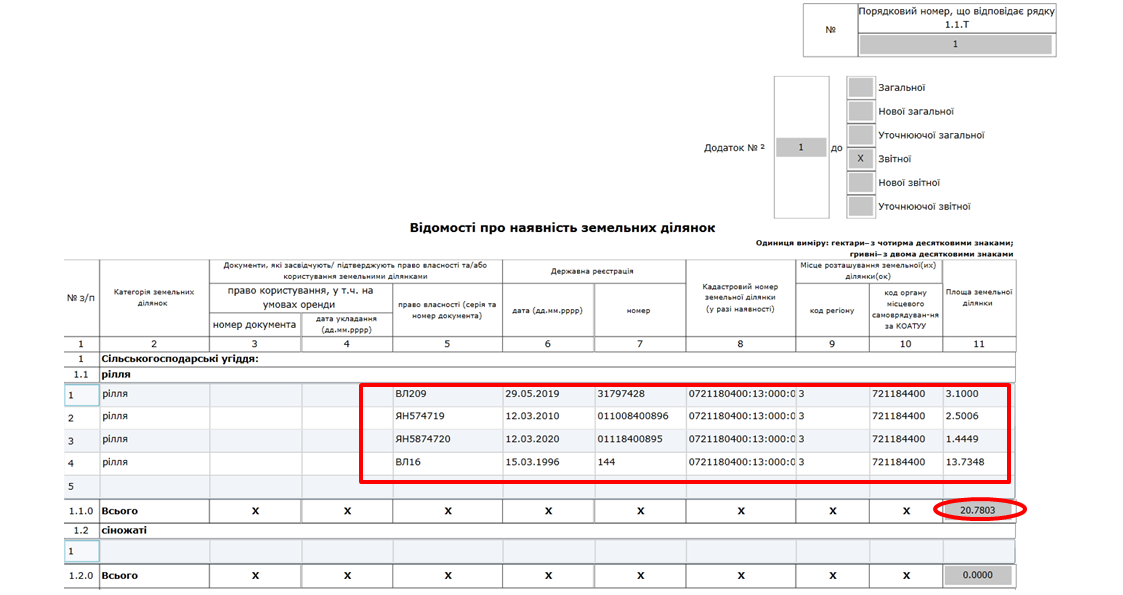

Importantly! Information on the availability of land plots is an integral part of general and reporting tax declarations of the single tax payer of Group IV.

Area of land plots specified in the Information must coincide with area declared in tax declaration of the single tax payer of Group IV, to which it is attached.

Information on the availability of land plots must contain information on each land plot in respect of which tax was accrued.

Such Information must contain data on the area of land plots, their location, cadastral numbers, information about documents confirming the ownership right or use of land plots, as well as information on state registration of such rights.

Reminder! Taxation object of the single tax payer of Group IV is area of agricultural land owned by agricultural producer or provided to him / her for use, including on lease.

Herewith, Articles 125 and 126 of the Land Code of Ukraine establish that the ownership right of land, as well as right of permanent use and land lease arise from the state registration of these rights issued according to the Law of Ukraine as of 01.07.2004 № 1952 “On state registration of real property rights and their encumbrances” (hereinafter – Law № 1952).

Right to lease land plot is subject to state registration according to the Law № 1952 and arises from the moment of state registration of such right.

Law of Ukraine as of 06.10.1998 № 161-XIV “On Land Lease” stipulates that land tenant is obliged to start using land plot within the terms established by the land lease agreement, but not before state registration of relevant lease right.

Article 211 of the Land Code of Ukraine stipulates that use of land without proper registration of rights, including lease, is a violation of land legislation.

Given above specified, the agricultural producers must include in taxation object of the single tax payer of Group IV the areas of agricultural land registered according to requirements of the Law № 1952 and amount of income of agricultural producers, namely income from the sale of agricultural products grown or produced on agricultural land, ownership or use of which (including lease) registered respectively to requirements of current legislation.

It is also mandatory to fill in the type of tax declaration to which land plots are attached, indicating relevant marks.

Group IV may be chosen by agricultural producers whose share of agricultural production for the previous tax (reporting) year is equal to or exceeds 75%.

Size of share must be reflected in the Calculation of agricultural production share, which is submitted to the controlling body with tax reporting of the single tax payer of Group IV within a period specified by tax legislation, namely not later than February 20 of current year. In 2022, as the deadline is a day off, the last day to submit is February 21, 2022.

Business entity in the Calculation of agricultural production share must fill in all necessary lines and make a reliable calculation according to the specified formulas. The following lines must be filled in:

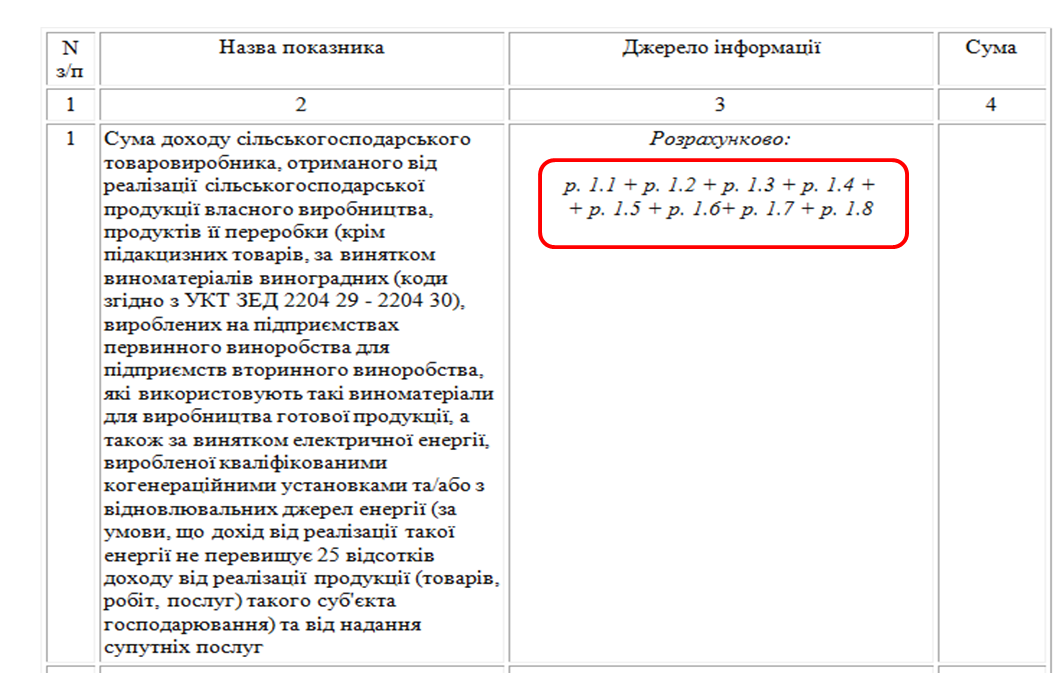

line 1 “Amount of income of agricultural producers received from the sale of agricultural products of own production, products of its processing and provision of related services” (hereinafter – amount of income), which includes the sum of lines 1.1, 1.2, 1.3, 1.4, 1.5, 1.6 , 1.7, 1.8;

line 2 “Total amount of income of agricultural producers”;

line 3 “Amount by which the total amount of income of agricultural producers is reduced”, which includes the sum of indicators of lines 3.1, 3.2, 3.3, 3.4, 3.5, 3.6;

line 4 “Adjusted income of agricultural producers” (hereinafter – adjusted income), which is defined as difference between the total amount of income of agricultural producers and amount by which the total amount of income is reduced;

line 5 “Share of agricultural production for the previous tax (reporting) year”, which is determined by the ratio of amount of income to adjusted income.

It should be noted the Law of Ukraine as of 30.11.2021 № 1914-IX “On Amendments to the Tax Code of Ukraine and other legislative acts of Ukraine to ensure balanced budget revenues” amended Section XIV of the Tax Code of Ukraine, which entered into force on 01.01.2022.

Second clause of Sub-paragraph 291.51.1of Paragraph 291.51Article 291 of the Code determines that business entities whose activities according to KVED-2010 (Classifier of economic activity types) belong to classes 01.47 (poultry breeding), 01.49 (in terms of breeding and rearing of quails and ostriches) and 10.12 (poultry meat production) may not be the single tax payers of Group IV.

Herewith, please note that business entities that simultaneously with other types of agricultural activity carry out activities according to KVED -2010, which belong to classes 01.47 (poultry breeding), 01.49 (in terms of breeding and rearing of quails and ostriches) and 10.12 (poultry meat production) also cannot acquire or confirm status of the single tax payer of Group IV for 2022.

Another reminder! Tax Code of Ukraine stipulates that business entities that as of January 1 of the base (reporting) year have a tax debt, except for bad tax debt, which arose due to force majeure (force majeure circumstances) may not be the single tax payers of Group IV.

Law of Ukraine as of 02.12.1997 № 671/97-VR “On Chambers of Commerce and Industry in Ukraine” stipulates that force majeure circumstances are extraordinary and unavoidable circumstances that objectively prevent fulfillment of obligations under the contract terms (contract, agreement, etc.), obligations under legislative and other regulations, namely: war threat, armed conflict or serious threat of such conflict, including but not limited to enemy attacks, blockades, military embargoes, actions of foreign enemy, general military mobilization, military action, declared and undeclared war, actions of public enemy, riots, acts of terrorism, sabotage, piracy, riots, invasion, blockade, revolution, revolt, uprising, mass riots, curfew, quarantine established by the Cabinet of Ministers of Ukraine, expropriation, forcible seizure, seizure of enterprises, requisition, public demonstration, blockade, strike, accident, illegal actions of third parties, fire, explosion, long breaks in the transport work, regulated by terms of relevant decisions and acts of public authorities, closure of sea channels, embargoes, ban (restriction) on exports / imports, etc., as well as caused by exceptional weather conditions and natural disasters, namely: epidemic, severe storm, cyclone, hurricane, tornado, storm, flood, snow accumulation, ice, hail, frost, freezing sea, straits, ports, passes, earthquakes, lightning, fire, drought, subsidence and landslides, other natural disasters, etc.

Chamber of Commerce and Industry of Ukraine and its authorized regional chambers of commerce and industry certify force majeure and issue a certificate of such circumstances within seven days from the date of the business entity’s appeal.

Agricultural producers be aware that in case of transition to the single tax payer’s Group III or independent refusal to register as the single tax payer of Group IV in connection with transition to the general taxation system, such business entity may re-elect the single tax payer’s Group IV not earlier than two calendar years after transition or refusal.

However, this rule is not applicable in case of registration cancellation of the single tax payer of Group IV at the initiative of controlling body.

In case of independent refusal to register as the single tax payer of Group IV during the tax (reporting) year (regardless of choice of another group or general taxation system), the agricultural producer is obliged to submit clarifying tax declaration of the single tax payer of Group IV in which such agricultural producer reduces accrual for quarters when he / she will not be the single tax payer of Group IV and must to fill in line 11 “Amount of tax liability of 25% of the annual amount of tax according to Sub-paragraph 298.8.7 of Paragraph 298.8 Article 298 Chapter 1 Section XIV of the Tax Code of Ukraine”.

This amount is a part of the single tax liability and calculated on the basis of 25% of the annual tax amount for each quarter during when taxpayer was in the single tax payer’s Group IV.

Example:

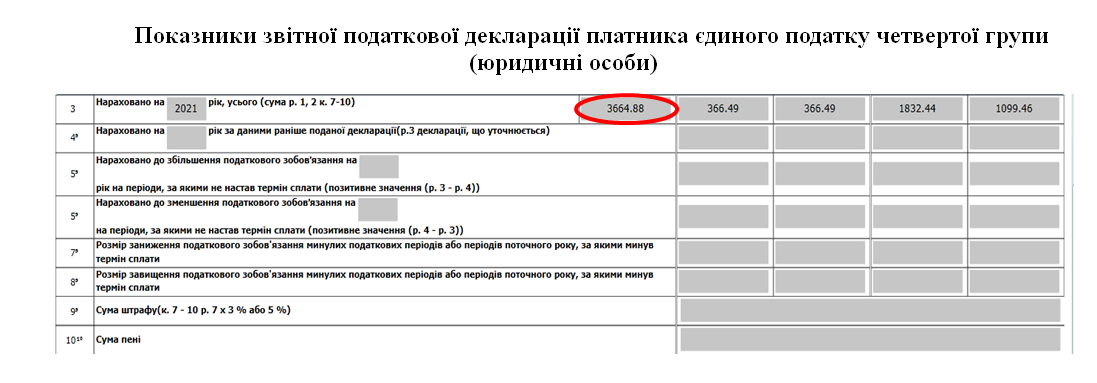

Agricultural producer submitted tax declaration of the single tax payer of Group IV (legal entity) to the controlling body and independently declared tax liabilities from the single tax for relevant year in the amount of 3 664.88 UAH.

Single tax payer of Group IV (legal entity) decided to transit to Group II of the single tax payer from any quarter of current year (in example: from the second quarter). Business entity in this case must submit the clarifying tax declaration of the single tax payer of Group IV, on the basis of which to declare for reduction the tax liabilities from the single tax for periods for which the due date has not come (for the second, third and fourth quarters of current year) and obligatory declare tax liabilities in the amount of 25% of the annual amount of tax for each quarter during which the taxpayer was in the single tax payer Group IV (for the first quarter of this year):

3 664.88 UAH * 25% = 916.22 UAH

Agricultural producer is obliged to submit clarifying general tax declaration of the single tax payer of Group IV to the controlling body at the main tax accounting place, as well as information on the availability of land, indicating general indicators of tax liabilities and general area of land belonging to payer.